Sand Batteries and Thermal Energy Storage: Viability, Economics, and Industrial Decarbonization Outlook

Decision-grade analysis of sand batteries, thermal storage economics, efficiency limits, vendors, and industrial heat use cases.

TL;DR

• Sand-based and related particulate sensible-heat thermal energy storage (TES) is commercially viable today as a heat-only technology for industrial process heat and district heating, but remains unproven and economically marginal as a power-to-power storage substitute for lithium-ion batteries. First-of-a-kind commercial systems, including Polar Night Energy's 1 MW / 100 MWh Pornainen plant (commissioned June 2025); Rondo Energy's 100 MWh Kern County, California unit (commercial operation October 2025); Magaldi/Enel's 7.5 MWh Buccino plant (September 2025); Brenmiller's 32 MWh Tempo Beverages unit (under commissioning); and Kyoto Group's 56 MWh KALL Ingredients molten-salt unit (October 2025), demonstrate that resistive electric charging of low-cost solid media to 500–1,500 °C, with heat-to-heat round-trip efficiencies of 90–97%, is now a deployable solution for decarbonising the roughly two-thirds of US industrial heat demand below 400 °C.

• The economics work where three conditions co-exist: (i) high carbon-priced gas (EU ETS averaged €65/t in 2024 and has fluctuated €60–80/t in 2025), (ii) frequent low priced or curtailed renewable electricity, and (iii) high-utilisation, long-life industrial heat loads. Vendor-reported installed capex for thermal storage averaged ~$232/kWh ₜₕ globally in BloombergNEF's May 2024 LDES survey, versus $304/kWh for 4-hour lithium ion; NREL's ENDURING particle-TES techno-economic analysis (Ma et al., NREL/CP 5700-79014, 2021) targets ~$2–4/kWh ₜₕ for the storage media plus containment at GWh scale before power-island costs. Power-to-power round-trip efficiency is fundamentally Carnot-limited to roughly 40–50 % at 1,200 °C (NREL ENDURING baseline 50 %; IRENA 2020 projects 40–65 % by 2030 for sensible → Rankine reconversion). C-suite buyers should treat any vendor claim of "90%+ round-trip efficiency" as a heat-to-heat metric only and not comparable to electrochemical battery RTE.

• Residential sand batteries are largely uneconomic and remain a hobbyist niche; commercial-building deployment is plausible only via district heating; the real strategic opportunity is industrial process heat and grid-balancing of long-duration variable renewable energy (VRE), where the LDES Council's Net-Zero Heat report estimates that including TES lifts cumulative LDES investment from $1.6–2.5 trillion (excluding TES) to $1.7–3.6 trillion by 2040, and global LDES capacity from 1–3 TW to 2–8 TW. Capital allocators and policymakers should prioritise: (1) C&I process-heat retrofits in Europe, where ETS exposure and high gas prices have made unsubsidised parity within reach; (2) US industrial sites paired with on-site solar PV where the IRA Section 48E ITC for thermal storage remains accessible despite the July 2025 One Big Beautiful Bill Act constraints; and (3) district heating in the Nordics and Baltics. Avoid premature exposure to power-to power thermal storage pure-plays.

Sand Batteries and Sensible-Heat Thermal Storage: A Decision Grade Assessment of Viability, Economics, and Strategic Implications

Key Findings

- Heat-to-heat versus heat-to-electricity efficiency must be disaggregated; vendor and media conflation is endemic. Resistive electric heating into solid media is near-100 % efficient (Joule heating), and heat extraction efficiency from a well-insulated silo can exceed 90–97 % (Polar Night Energy's industrial-scale unit reports approximately 90% at the 100 MWh scale; Kraftblock claims >95%; Rondo claims >97%; Brenmiller claims ~97%). However, when the same stored heat is reconverted to electricity via a Rankine or Brayton cycle, the second-law (Carnot) limit drops effective round-trip efficiency to 25–50 %. NREL's ENDURING design baseline is 50% at 1,200 °C hot / 300 °C cold using an Air-Brayton Combined Cycle; IRENA's 2020 Innovation Outlook: Thermal Energy Storage projects molten-salt CSP heat-to-power RTE to rise from 45–50% in 2018 to 40–65% by 2030. The early Kankaanpää sand battery (2022) reports approximately 60–70w% overall, but as a heat-only system, not power-to-power.

- Sand is a credible storage medium with peer-reviewed validation, but "sand battery" is a marketing term covering very heterogeneous architectures. Silica sand has specific heat capacity of approximately 700–800 J/kg·K, bulk density approximately 1,500–1,800 kg/m³, and (per Davenport et al., Solar Energy 262: 111908, 2023) is thermally stable at 1,200 °C for at least 500 hours, with volumetric energy density of approximately 340 kWh ₜₕ /m³ at Δ T = 900 °C in NREL's ENDURING design. Polar Night Energy now uses crushed soapstone (better thermal conductivity than builders' sand) at 500–600 °C; Magaldi uses fluidised silica sand up to 550-1,000 °C; Brenmiller uses crushed rock to 650 °C; Rondo Energy uses refractory bricks (not sand) to 1,000–1,500 °C; MGA Thermal uses miscibility-gap alloy blocks to 600–700 °C; Antora uses carbon blocks to 1,800–2,400 °C. Across these, the underlying physics (sensible heat in cheap, abundant solid media) is sound, but the bill of materials, temperature regime, and discharge mechanism differ materially.

- The reference commercial deployments now exist and have published technical specifications. Verified operating installations as of May 2026 include:

- Polar Night Energy – Vatajankoski, Kankaanpää, Finland (200 kW / 8 MWh, 100 tons builders' sand, operating since 2022—the first commercial sand-based district-heating battery).

- Polar Night Energy – Loviisan Lämpö, Pornainen, Finland (1 MW / 100 MWh, 2,000 t crushed soapstone, 500 °C, 13 m × 15 m, commissioned June 2025; covers approximately one month of summer / one week of winter Pornainen heat demand; expected to cut local district heating CO₂ by approximately 68 %).

- Polar Night Energy – Lahti Energia, Vääksy, Finland (2 MW / 250 MWh contracted November 2025).

- Rondo Energy – Holmes Western Oil Corp., Kern County, California (100 MWh, refractory brick, >1,000 °C, 20 MW co-located solar PV, claimed >97 % heat-to-heat RTE, commercial operation October 2025—the largest operating industrial heat battery).

- Brenmiller Energy – SUNY Purchase, New York (commissioned with NYPA; captures gas turbine exhaust into crushed rock; won POWER 2025 C&I Generation Award) and a 32 MWh bGen unit under installation at Tempo Beverages, Israel (Heineken-affiliated), expected to displace 6,200 t CO₂/yr and save $7.5 million over 15 years.

- Magaldi/Enel MGTES – I.GI., Buccino, Italy (7.5 MWh fluidised-sand thermal battery, inaugurated 16 September 2025, approximately 500 t CO₂/yr avoided).

- MGA Thermal – Tomago, NSW (5 MWh demonstrator, 3,700 MGA blocks, 500 kW resistive heating, generating 365 °C / 37 bar steam, completed 2025 with ARENA backing).

- Kyoto Group – KALL Ingredients, Tiszapüspöki, Hungary (56 MWh molten-salt Heatcube, 14 MW discharge, inaugurated October 2025).

- Capital cost data are predominantly vendor-reported. BloombergNEF's May 2024 LDES survey put fully-installed thermal storage system capex at a global average of $232/kWh versus $304/kWh for 4-hour lithium-ion and $293/kWh for compressed air. Independent academic work (Ma et al., NREL/CP-5700-79014, 2021) indicates that the storage media plus containment component for silica-sand systems can fall to approximately $2/kWh ₜₕ at large scale, but installed system costs including resistive heaters, heat exchangers, and (where relevant) power-cycle equipment are an order of magnitude higher. IRENA (2020) projected sensible TES costs to fall from approximately $35/kWh in 2018 to approximately $25/kWh by 2030, and the US DOE Long Duration Storage Shot target of $0.05/kWh LCOS by 2030 is not yet met by any thermal storage configuration in DOE's August 2024 review.

- Residential sand batteries are not currently a defensible investment thesis. Sensible heat storage exhibits surface-area-to-volume losses that scale unfavourably with size: small systems lose proportionally more heat. The few residential vendors (e.g., Batsand) market 8–10 year paybacks contingent on combination with rooftop solar and on the avoidance of grid power for heating during a transition off gas; these are not independently validated. The economics fail in most contexts because (a) heat pumps deliver 3–4× COP versus sand batteries' 1× resistive heating, (b) hot-water tank storage is two orders of magnitude cheaper for the temperature regime needed in dwellings, and (c) the residential heat load profile (peaks of 12–24 hours) does not require the multi-day duration where sand storage excels.

- Commercial deployment is gated by the presence of an existing district-heating network or a sizable, contiguous, high-utilisation heat load. In the Nordics, Germany, the Baltics, and parts of Eastern Europe, district heating networks reach 50–95% of urban heat demand; this is where Polar Night Energy and Kyoto Group are gaining traction. In North America, the absence of district heating constrains commercial-tier deployment to campus, hospital, and prison microgrids (where Brenmiller's SUNY Purchase deployment is the marquee reference), which are markets too small to absorb the volumes implied by the LDES Council's TW-scale forecasts.

- Industrial process heat is the genuine strategic opportunity, and is the use case where vendors have the strongest deployment evidence. Industrial heat accounts for more than 20% of global final energy consumption (McKinsey, Net-zero electrical heat, 2024), approximately 90% of which is currently met with fossil fuels (LDES Council / McKinsey Net-Zero Heat, COP27, 2022). Approximately two-thirds of US industrial process heat is below 300 °C (NREL/JISEA, McMillan, 2019), the regime served by Polar Night Energy, Brenmiller, Kyoto Group, EnergyNest, and Magaldi. The 400–1,500 °C regime is addressed by Rondo Energy (brick), Antora (carbon), Kraftblock (recycled-slag composite), and MGA Thermal. The Renewable Thermal Collaborative and McKinsey identify process-heat decarbonisation as the next industrial decarbonisation frontier.

- Supply chain and materials sovereignty are a genuine strategic advantage relative to lithium-ion. Sand, crushed rock, soapstone, refractory brick, recycled steel slag, and concrete are abundant, non-critical, non-toxic, non-flammable, and locally sourceable in virtually every jurisdiction. There is no analogue to the lithium-cobalt-nickel-graphite criticality stack. Brenmiller and Kraftblock specifically use upcycled industrial by-products (crushed rock, steel slag), aligning with circular-economy procurement frameworks (e.g., EU Critical Raw Materials Act).

- Policy treatment is favourable but inconsistent. In the EU, thermal storage qualifies for Innovation Fund support, national Carbon Contracts for Difference (Germany's Klimaschutzverträge, Netherlands SDE++), and the announced Clean Industrial Deal and Industrial Decarbonisation Accelerator Act. The forthcoming approximately €1.2 billion EU pilot auction to decarbonise industrial process heat (cited by Brenmiller leadership) is the largest single demand-side instrument. In the US, the IRA's Section 48 and 48E ITC explicitly cover thermal energy storage property as standalone-eligible (per IRS final regulations, January 2025); the Office of Clean Energy Demonstrations had committed up to $75 million to Rondo–Diageo projects. The One Big Beautiful Bill Act (July 2025) terminated the 2% energy credit for thermal storage and introduced PFE/FEOC restrictions but preserved Section 48E eligibility for thermal storage. In the UK, the Cap-and-Floor scheme will become the dominant LDES procurement instrument from 2027.

- The LDES Council's 50× scale-up call frames thermal storage as the marginal LDES capacity-creator. Per the LDES Council's Net-Zero Heat report (2022) and 2024 Annual Report, the inclusion of TES expands global plausible LDES capacity by 2040 from 1–3 TW to 2–8 TW, lifting cumulative investment from $1.6–2.5 trillion (without TES) to $1.7–3.6 trillion (with TES). The Council projects power capex for steam-discharge TES to fall 15–30% by 2040 and energy capex by 25–70%.

Details

1. Technology and Engineering Fundamentals

Physics. Heat storage relies on Q = m·c ₚ · Δ T, where the storage medium's mass (m), specific heat capacity (c ₚ ), and operating temperature range ( Δ T) determine energy content. For silica sand, c ₚ ≈ 0.7–0.8 kJ/kg·K and bulk density ≈ 1,500–1,800 kg/m³, yielding volumetric energy density of approximately 150–340 kWh ₜₕ /m³ depending on Δ T. This is roughly an order of magnitude less than lithium-ion (approximately 300 kWh/m³ electrical, 1.08 GJ/m³), but the cost differential is 2,000–2,500× in favour of sand at the medium level (Stanford PH240/Schreiner, 2025), inverting the calculus for stationary heat applications. Davenport et al. (Solar Energy 262: 111908, 2023) demonstrated silica sand thermal stability at 1,200 °C for 500 hours with no degradation, validating its candidacy for high-temperature TES.

Storage media and operating temperatures: Five media classes have reached commercial or pre-commercial deployment:

• Builders / silica sand: Polar Night Energy first generation (Kankaanpää), Magaldi (fluidised); 500–1,000 °C.

• Crushed soapstone: Polar Night Energy Pornainen (a Tulikivi manufacturing by product); approximately 500 °C.

• Crushed rock / aggregate: Brenmiller bGen; ≤650 °C.

• Refractory brick: Rondo Energy; 1,000–1,500 °C.

• Engineered composites: MGA Thermal miscibility-gap alloy blocks (graphite matrix with embedded aluminium / magnesium / copper / zinc alloy particles, latent-plus-sensible) to 650 °C; Kraftblock recycled-slag composite to 1,300 °C; Antora solid carbon blocks to 1,800–2,400 °C; EnergyNest's HEATCRETE® (proprietary concrete developed with HeidelbergCement) to approximately 390 °C.

Charge/discharge architecture. All commercial systems use electric resistive (Joule) heating elements either embedded within the storage medium or in a closed gas loop circulating through it. Charging is essentially 100% efficient electrically. Heat extraction uses air (Polar Night Energy, Rondo), steam directly (Brenmiller, MGA Thermal, Kraftblock, Kyoto Group), thermal oil (EnergyNest), or thermophotovoltaic conversion (Antora, the only commercial system targeting heat-to-electricity directly).

Round-trip efficiency — disaggregated.

• Heat-to-heat (electric → heat → heat delivered): 85–97% is achievable and is what most vendors cite. Vatajankoski's first-generation 8 MWh unit reported approximately 60–70% due to small-scale parasitic losses; Polar Night Energy claims annual efficiency of 85% at small scale rising above 90% at the 100 MWh Pornainen scale; Rondo claims >97% at 100MWh; Kyoto Group claims 93% at 56 MWh; Brenmiller and Kraftblock each cite approximately 97% and >95% respectively.

• Heat-to-electricity (power-to-power): fundamentally Carnot-limited. NREL ENDURING's design baseline is 50% at 1,200 °C with an Air-Brayton Combined Cycle (Ma et al., NREL/CP-5700-79014, 2021). IRENA (2020) projects 40–65% by 2030 for advanced cycles; the lower end (25–40%) applies to lower-temperature systems with Rankine cycles. Magaldi's MGTES self-reports >90% for heat applications but only 35–45% for electricity generation, a vendor figure that confirms the physics rather than refuting it.

Self-discharge and thermal retention. Magaldi reports MGTES thermal losses <2%/day; EnergyNest reports approximately 2%/day. Polar Night Energy's larger silo retains heat for months given proper insulation and an improving surface-to-volume ratio at scale. This positions sand storage as a days-to-weeks duration technology in its current commercial form, not a seasonal storage technology, although Polar Night Energy claims summer-charging-for-winter discharge is feasible with the Pornainen architecture.

Footprint. The Pornainen unit is 13 m tall × 15 m wide for 100 MWh; Polar Night Energy's standard 1,000 MWh modular product would occupy roughly the footprint of a small substation. Rondo's 100 MWh unit is comparable to a four-story prefabricated office building. Footprints are larger per kWh than lithium-ion but smaller than pumped hydro and comparable to or smaller than compressed air storage.

Lifespan. Vendor specifications cluster around 25–30+ years (EnergyNest, Magaldi, Polar Night Energy), with the storage medium itself being effectively non-degrading; the heating elements and heat-exchanger tubing are the lifecycle-limiting components and are standard replaceable industrial parts. Lithium-ion battery storage in comparison degrades materially over 10–15 years.

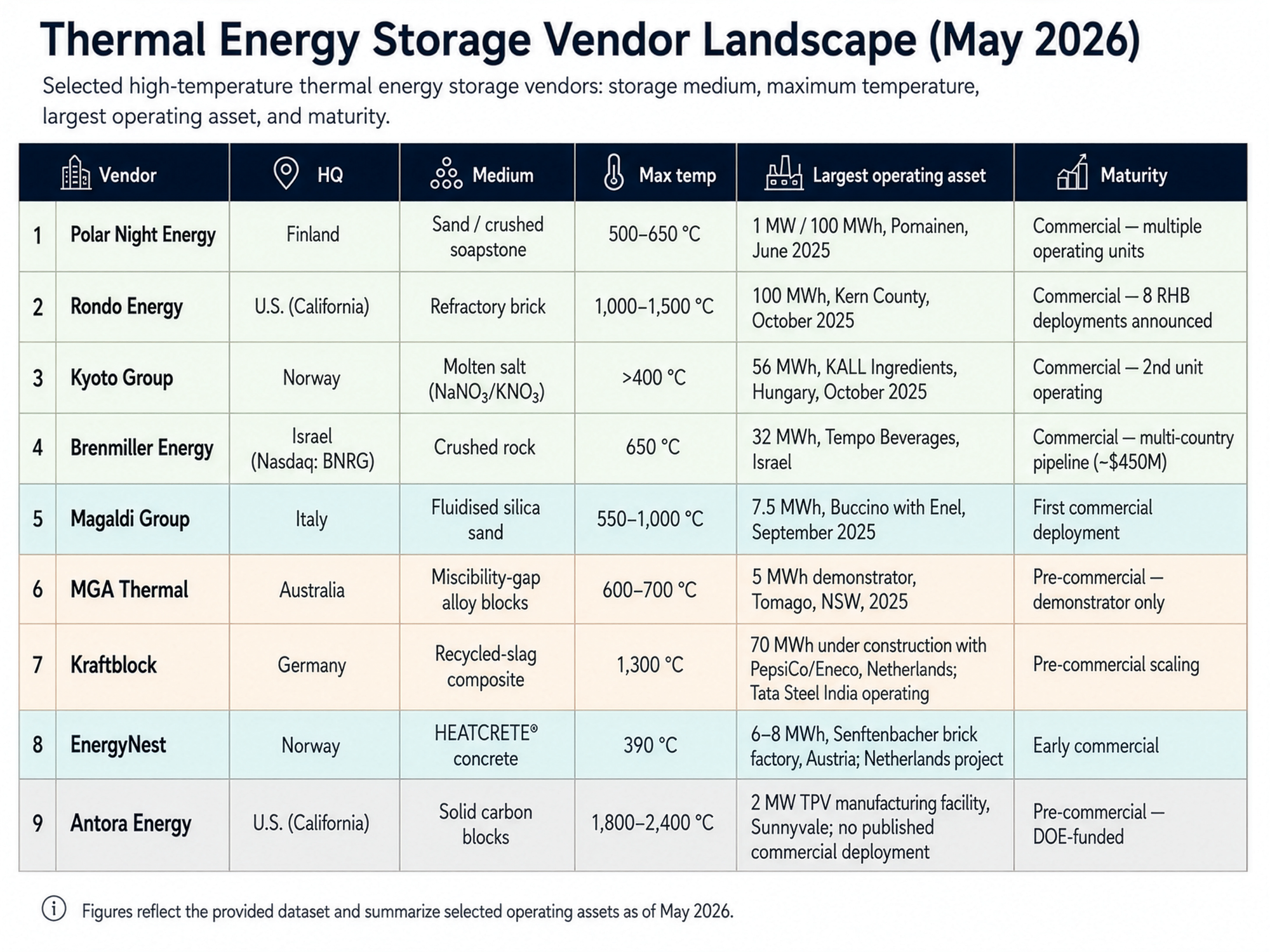

2. Key Players and Maturity Assessment

| Vendor | HQ | Medium | Max Temp | Largest Operating Asset (May 2026) | Maturity |

|---|---|---|---|---|---|

| Polar Night Energy | Finland | Sand / crushed soapstone | 500–650 °C | 1 MW / 100 MWh, Pornainen, June 2025 | Commercial — multiple operating units |

| Rondo Energy | US (California) | Refractory brick | 1,000–1,500 °C | 100 MWh, Kern County, October 2025 | Commercial — 8 RHB deployments announced |

| Kyoto Group | Norway | Molten salt (NaNO3 / KNO3) | >400 °C | 56 MWh, KALL Ingredients, Hungary, October 2025 | Commercial — second unit operating |

| Brenmiller Energy | Israel (Nasdaq: BNRG) | Crushed rock | 650 °C | 32 MWh, Tempo Beverages, Israel | Commercial — multi-country pipeline ~$450M |

| Magaldi Group | Italy | Fluidised silica sand | 550–1,000 °C | 7.5 MWh, Buccino with Enel, September 2025 | First commercial deployment |

| MGA Thermal | Australia | Miscibility-gap alloy blocks | 600–700 °C | 5 MWh demonstrator, Tomago, NSW, 2025 | Pre-commercial — demonstrator only |

| Kraftblock | Germany | Recycled-slag composite | 1,300 °C | 70 MWh under construction with PepsiCo / Eneco Netherlands; Tata Steel India operating | Pre-commercial scaling |

| EnergyNest | Norway | HEATCRETE concrete | 390 °C | 6–8 MWh, Senftenbacher brick factory, Austria; Netherlands project | Early commercial |

| Antora Energy | US (California) | Solid carbon blocks | 1,800–2,400 °C | 2 MW TPV manufacturing facility, Sunnyvale; no published commercial deployment | Pre-commercial — DOE-funded |

Credibility filter. Only Polar Night Energy, Rondo Energy, Kyoto Group, Brenmiller Energy, and Magaldi Group meet a rigorous bar of "operating commercial-scale installation with named offtaker and published capacity." MGA Thermal, EnergyNest, Kraftblock, and Antora have demonstrators or first-of-kind units but limited or no fully-commercial revenue assets. Antora, despite a $150 million Series B (2024), has no publicly named commercial deployment delivering process heat to a third-party customer as of May 2026.

3. Economics

Capex.

• BloombergNEF (May 2024): global average installed TES capex $232/kWh; CAES $293/kWh; 4-hour lithium-ion $304/kWh; gravity storage $643/kWh.

• IRENA (2020): sensible TES industry-tier capex projected to fall from $35/kWh (2018) to $25/kWh (2030).

• NREL ENDURING (Ma et al. 2021, NREL/CP-5700-79014): silica sand storage media + containment approximately $2/kWh ₜₕ at GWh scale; full system $2–4/kWh ₜₕ before power island costs.

• Kraftblock (vendor): sensible heat materials below $35/kWh ₜₕ for rocks/ceramics.

• Vendor-reported residential (Batsand): 8–10 year payback

Operating costs. Negligible compared to fossil-fuel boilers; the dominant opex is the cost of charging electricity. Polar Night Energy and Rondo both use algorithmic charging targeting the six lowest-cost hours per day. In markets with frequent negative or sub-$10/MWh hours (Iberia, Nordics, Texas, California middays), this is a structural advantage; in markets with flat retail tariffs and no demand-response, the value proposition collapses.

Levelised cost. No independently-verified LCOS for sand-based systems exists in the public peer-reviewed literature; the DOE Long Duration Storage Shot 2030 target is $0.05/kWh LCOS, and DOE's August 2024 review concluded no thermal storage configuration currently meets this. Brattle (cited via Generate Capital) projects unsubsidised TES heat delivery below $6/MMBtu by 2030 under favourable conditions—competitive with $5–8/MMBtu industrial natural gas in most markets.

Comparative analysis.

• Versus lithium-ion: heat-only sand TES is 2–10× cheaper per kWh ₜₕ for stationary heat applications. Lithium-ion remains dominant for power-to-power short-duration applications and is the wrong tool for industrial process heat.

• Versus molten salt: sand and brick systems eliminate corrosion, freezing-point, and heat tracing risks that plague molten-salt CSP plants; sand has higher max operating temperatures (1,200 °C vs. approximately 565 °C for solar salt).

• Versus hot-water tanks: sand systems can operate 5–10× hotter, store an order of magnitude more energy per m³, and discharge as steam directly, eliminating the boiler.

• Versus heat pumps: heat pumps achieve COP 3–4 versus 1 for resistive sand-charging, making them more efficient for low-temperature space heating (<80 °C). Sand batteries become competitive only above approximately 150 °C, where heat-pump efficiency collapses, and in time-shifting roles where the heat pump must be supplemented by storage.

Payback. Vendor-cited paybacks: Tempo Beverages ($7.5 million savings over 15 years on 32 MWh Brenmiller deployment. SUNY Purchase) Brenmiller meets approximately 100% of building heat needs and approximately 50% of electricity. These are project-specific and exclude IRA/Innovation Fund grants that typically offset 20–40% of capex.

4. Regulatory and Policy Landscape

United States. Section 48 (legacy) and 48E (technology-neutral, post-2024 construction) of the Internal Revenue Code, as amended by the IRA, explicitly classify thermal energy storage property as standalone-eligible for the 6%/30% Investment Tax Credit (with prevailing-wage and apprenticeship adders bringing it to 30–50 %). IRS final regulations (January 2025) confirmed that thermal storage qualifies and clarified eligible property lists. The One Big Beautiful Bill Act (July 4, 2025) introduced Prohibited Foreign Entity restrictions and removed certain MACRS classifications but preserved 48E for thermal storage. DOE's Office of Clean Energy Demonstrations had negotiated up to $75 million for Rondo–Diageo projects (status: under discussion as of October 2025).

European Union. Thermal storage is eligible under the Innovation Fund, the announced Industrial Decarbonisation Accelerator Act, the Clean Industrial Deal, and national CCfD schemes (Germany's Klimaschutzverträge, Netherlands SDE++). The EU ETS averaged €65/t in 2024 and has fluctuated €60–80/t in 2025 (European Commission, Special Issue on EU ETS macroeconomic impacts, November 2025), making industrial gas combustion progressively uneconomic and serving as the dominant driver of European industrial demand for thermal storage. CBAM (Carbon Border Adjustment Mechanism) reinforces this for exporters. The Energy Performance of Buildings Directive (revised April 2024) targets a fully decarbonised building stock by 2050, indirectly supporting district-heating TES.

United Kingdom. The Cap-and-Floor scheme (currently being designed for LDES, expected to procure first-of-a-kind LDES from 2027) is the most explicit dedicated LDES procurement mechanism globally.

Nordics. Finland and Sweden have integrated district-heating subsidies and innovation grants (Business Finland funded the Pornainen project). Sweden's carbon tax reached 1,450 Swedish crowns (€126) per tonne of CO₂ in 2024 (European Parliament Research Service brief EPRS_BRI(2024)767174), the highest globally, making the Polar Night Energy and Vatajankoski deployments economic without further subsidy.

Australia. ARENA funded MGA Thermal's demonstrator with an initial A$1.27 million grant announced 10 August 2022 by Energy Minister Chris Bowen; a further A$2.48 million was added after the 2023 overheating incident, bringing total ARENA funding to A$3.75 million.

5. Geopolitical and Strategic Dimensions

Materials sovereignty. Sand, crushed rock, refractory brick, soapstone, and recycled steel slag are abundant globally. The total bill of materials for a 100 MWh sand battery includes no critical raw materials as defined by the EU Critical Raw Materials Act or US DOE Critical Materials Assessment. This contrasts sharply with lithium-ion (lithium, cobalt, nickel, graphite, manganese), vanadium flow batteries (vanadium), and even compressed-air systems (specialty turbomachinery).

Energy security. The 2022 European gas crisis catalysed industrial-buyer interest in electrified heat with on-site storage as a hedge against fossil-fuel supply disruption. Polar Night Energy, Brenmiller, Kraftblock, and Kyoto Group have all publicly attributed pipeline acceleration to post-2022 demand. Rondo's CEO has cited European utilities' "very engaged" interest as a function of the gas-price differential between Europe and the US.

Country positioning.

• Finland: the global epicentre of sand-battery deployment, exploiting district heating infrastructure (~50 % of Finnish heat demand), high renewables penetration, and a domestic supply chain (Tulikivi soapstone, Vatajankoski utility partnership).

• Israel: Brenmiller Energy is publicly listed (Nasdaq: BNRG) and has secured a $450 million project pipeline, with approximately 50% in Europe.

• Germany: Kraftblock anchors the German position, with Series B backers including Shell, ArcelorMittal-funded Finindus, and Spanish A&G; Tata Steel is operating its system in Jamshedpur.

• United States: Rondo and Antora lead, with Energy Impact Partners, Microsoft, Aramco, Rio Tinto, SABIC, SDCL, Siam Cement, and Breakthrough Energy Ventures funding the segment.

• Australia: MGA Thermal with ARENA and Shell backing; first-of-kind demonstrator in NSW.

• Italy: Magaldi-Enel partnership rooted in CSP heritage; first MGTES at Buccino

6. LDES Context

The LDES Council's 2024 Annual Report calls for global LDES capacity of 1–1.5 TW by 2030 and 8 TW by 2040, a 50× acceleration from the current 0.22 TW deployment pipeline against 115 GW installed (2023). The Council estimates this represents a $4 trillion cumulative investment opportunity with potential annual system savings of $540 billion. The Council's Net-Zero Heat report (COP27, November 2022) and December 2024 thermal-focused publication conclude that the inclusion of TES could increase plausible 2040 LDES capacity from 1–3 TW to 2–8 TW—i.e., TES is the marginal expansion driver, lifting cumulative investment from $1.6–2.5 trillion (without TES) to $1.7–3.6 trillion (with TES). BloombergNEF, IDTechEx, and IRENA all corroborate that thermal storage is structurally cheaper than electrochemical alternatives for durations exceeding ~8 hours.

DOE's Long Duration Storage Shot targets $0.05/kWh LCOS by 2030; DOE's August 2024 review finds molten-salt thermal storage can achieve a potential 17% LCOS reduction (smallest of all LDES categories evaluated) but did not assess sand or solid-particle systems specifically. NREL's ENDURING project achieved its design milestones and signed an IP option with a US manufacturer, with $5.5 million in follow-on DOE funding to support continued development.

Recommendations

For institutional investors.

- Prioritise C&I industrial process-heat projects in Europe with named offtakers, high gas displacement, and policy-backed revenue (CCfD, Innovation Fund, SDE++). Polar Night Energy, Rondo, Kyoto Group, Brenmiller, and Kraftblock are the leading deployment vehicles. Expected payback 5–8 years unsubsidised in high-ETS markets; 3–5 years subsidised.

- Avoid power-to-power thermal storage pure-plays until at least one independently-verified commercial system demonstrates >40 % round-trip efficiency at scale. NREL's ENDURING and Antora's TPV technology remain pre-commercial. The $0.05/kWh LCOS bar for grid arbitrage is not met.

- Treat residential sand-battery offerings as venture-grade speculation; heat pumps with conventional hot-water storage will outcompete in nearly all residential cases.

- Threshold for re-evaluation: if any vendor publishes audited round-trip efficiency >50% electric-to-electric at >50 MWh commercial scale, the power-to-power thesis warrants reopening.

For C-suite executives at energy-intensive industrials.

- Conduct site-by-site assessment of process-heat demand, temperature profile, capacity factor, gas-price exposure, and access to low-cost off-peak electricity. The shortest paybacks occur at facilities with >70 % capacity factor, gas costs >€40/MWh ₜₕ , and access to electricity below €30/MWh at least 6 hours/day.

- Negotiate Heat-as-a-Service contracts where capex risk transfer matters: Brenmiller, Kyoto Group, and Polar Night Energy all offer 12–25-year HaaS structures, removing capex from the balance sheet.

- Use sand TES as a hedge, not a primary asset: pair with retained gas/biomass peaking capacity (as Loviisan Lämpö retained woodchip backup at Pornainen) to manage outage risk during commissioning years.

- Benchmark to threshold: if internal cost of CO₂ avoidance exceeds €60–80/t (around current EU ETS range), TES is in the money; if below €40/t, defer.

For policymakers.

- Explicitly include thermal storage in LDES procurement schemes on parity with electrochemical and mechanical storage. The UK Cap-and-Floor model is the strongest current precedent; replicate in EU industrial-decarbonisation bank instruments.

- Design grid tariff structures (time-of-use, demand-response, negative-price passthrough) to reward flexible electric heating loads.

- Direct concessional capital (Innovation Fund, IRA-derived DOE OCED, Australian ARENA, UK NESO) to first-of-a-kind C&I deployments where the value-of-information is highest.

- Threshold for policy escalation: if 2027 capex data shows installed cost <$150/kWh ₜₕ at 50+ MWh scale, expand TES-specific procurement.

For corporate strategists in incumbent energy/utility sectors.

- Partner before acquiring: Enel-Magaldi, EDP-Rondo, Eneco-Kraftblock, Loviisan Lämpö Polar Night Energy, NYPA-Brenmiller, and Lahti Energia–Polar Night Energy demonstrate the partnership template.

- Evaluate TES against electrolyser-plus-H ₂ for heat decarbonisation: TES generally wins below 600 °C; H₂ wins above 1,200 °C; the contested 600–1,200 °C band depends heavily on hydrogen pricing.

- Threshold for shift: if any single sand-TES vendor surpasses 1 GWh cumulative deployment globally by end-2026, treat as inflection point for sector consolidation.

Caveats

- Vendor data dominates the cost record. Outside BloombergNEF's 2024 LDES survey and IRENA's 2020 Innovation Outlook, very few independently-audited capex/LCOS datapoints exist for sand-based systems. Vendor claims of >97% round-trip efficiency (Rondo) and approximately 90% at 100 MWh scale (Polar Night Energy) have not been independently verified across full operating years, although the underlying physics supports them as plausible

- First-of-a-kind cost-overrun risk is unquantified. All five marquee commercial systems were commissioned in 2024–2025; multi-year operational data is unavailable.

- Heat-to-heat vs heat-to-power conflation is endemic in media coverage and some vendor marketing. Many articles describe a 90%+ "round-trip efficiency" without specifying that this is heat-to-heat; reading at face value would materially mislead a capital allocator.

- Antora's TPV-based heat-to-electricity claim of >40 % conversion efficiency is a vendor figure and represents a record claim rather than independently-replicated published result; thermophotovoltaic conversion at commercial scale is not yet proven.

- The DOE Long Duration Storage Shot target ($0.05/kWh LCOS by 2030) is, according to DOE's own August 2024 review, unlikely to be met by any technology absent further innovation; sand and brick TES are not the closest to the target.

- Power-to-power round-trip economics depend on charging electricity cost. With electricity at €0/MWh during oversupply hours and €100/MWh during scarcity hours, even 30% RTE can be economic; absent that spread, no thermal storage power-to-power application makes sense.

- The "world's largest" superlative has changed three times in 2025 (Polar Night Energy June, Kyoto Group October, Rondo October), reflecting genuine market acceleration but also a degree of marketing competition; the comparison is also apples-to-oranges (sand vs molten salt vs brick).

- Residential market sources in this report (Batsand, DIY communities) are commercial websites and hobbyist communities, not peer-reviewed or independently audited; the residential proposition should be treated as not currently validated.

- Geopolitical/policy risk: the One Big Beautiful Bill Act of July 2025 introduced ambiguity into the US thermal-storage ITC trajectory; further legislative changes could impair the US market within the investment horizon.

- Sand availability paradox: while sand is abundant globally, industrial-grade construction sand has well-documented supply pressures in some markets (per UNEP, Sand and Sustainability, 2022); the volumes required by even a 1 TW global TES build-out remain modest relative to construction-sector consumption, but local sourcing should be verified.