Shanghai Sinyang (SZSE:300236): A Wet-Chemicals Compounder Priced as a Photoresist Bet

Sinyang's copper-plating and wet-clean franchise drives real earnings; its ArF photoresist is qualification-stage optionality, not scaled revenue.

TL;DR

- Sinyang is an industrious profitable Chinese electronic-materials incumbent whose core copper-plating, wet-cleaning and etching chemistries are significant revenue engines (FY2025 revenue RMB 1.937bn, +31.28%; net profit RMB 301m, +71.12%); its photoresist franchise, by contrast, is qualification-stage optionality; KrF is in volume sale, but ArF is still overwhelmingly in customer certification, not material revenue.

- The bull case (localization tailwinds, 90–14nm copper-interconnect incumbency at Chinese fabs, low top-5 customer concentration of 37.97% in 2024, and rumored Japanese photoresist export curbs) is offset by a bear case centered on photoresist commercialization risk, a rich valuation (~59–70x trailing P/E in mid-2025, higher in 2026), and reported-earnings noise from its legacy stake in wafer maker National Silicon Industry Group (SHA:688126).

- English sell-side coverage is essentially nonexistent; the verifiable opinion record is mainland Chinese (Guotai Haitong "Overweight," target RMB 104.25 as of the Q1-2026 note) plus Eastmoney/aggregator consensus. Treat all price targets as thinly sourced and China-domestic.

Note:

This article was written on request; it is an investment focused analysis of a specific company. This is not a tech discussion. This is not financial advice. All information within should be independently verified and may not relied upon for investment decisions!

Shanghai Sinyang Semiconductor Materials Analysis - Photoresist Market

Key Findings

1. Company baseline: Shanghai Sinyang Semiconductor Materials Co., Ltd. (上海新阳半导体材料股份有限公司) trades as SZSE:300236 on the Shenzhen ChiNext board. It was founded July 1, 1999 and IPO'd June 29, 2011. The business is now organized as "one body, two wings": (a) a semiconductor / IC materials arm - electroplating solutions and additives (damascene copper, TSV), wafer cleaning chemistries, dry-etch post-clean, etchants, CMP slurry, photoresists, and supporting wet-process equipment; and (b) an environmental coatings arm (PVDF fluorocarbon and heavy-duty anticorrosive coatings) run through subsidiary Jiangsu Kopper. In 2024 the semiconductor segment was 70.19% of revenue and coatings 29.81%; by FY2025 semiconductor had risen to ~78% (RMB 1.5bn) and coatings fell to ~21.6% (RMB 4.19bn).

2. Financials show operating acceleration plus non-operating noise.

- FY2022: revenue RMB 1.196bn (+17.64%); net profit to parent RMB 53.23m (−43.16%); recurring (扣非) net profit RMB 111.61m (+31.74%). The reported net-profit decline was attributed by the company mainly to fair-value changes.

- FY2023: revenue RMB 1.212bn (+1.4%); net profit RMB 166.84m (+213.41%); recurring net profit only RMB 123.07m (+10.27%). The 213% headline is a low-base effect (2022's fair-value drag reversing) plus non-recurring items, not an operating tripling.

- FY2024: revenue RMB 1.475bn (+21.67%); net profit RMB 175.71m (+5.32%); recurring net profit RMB 160.77m (+30.63%); gross margin 39.29%; R&D RMB 220m (14.92% of revenue). Semiconductor revenue RMB 1.035bn (+34.78%).

- H1 2025: revenue RMB 897m (+35.67%); net profit RMB 133m (+126.31%); recurring net profit RMB 127m (+58.07%).

- Q1–Q3 2025: revenue RMB 1.394bn (+30.62%); net profit RMB 211m (+62.70%); recurring RMB 197m (+53.01%).

- FY2025: revenue RMB 1.937bn (+31.28%); net profit RMB 301m (+71.12%); recurring RMB 274m (+70.48%); semiconductor GM 45.88%; IC-materials sales volume 28,500 tons (+45%); government subsidies of RMB 40.88m boosted profit.

- Q1 2026: revenue RMB 577m (+33.05%); net profit RMB 103.81m (+103.11%); recurring RMB 98.89m (+109.52%).

3. The silicon-wafer stake is a legacy asset, now marked through equity not profit. Sinyang co-founded 300mm-wafer pioneer Shanghai Xinsheng (上海新昇) in 2014 alongside Xingsen Technology and the Richard Chang (张汝京) team, under China's "02 Special Project." It lost control when National Silicon Industry Group (沪硅产业, SHA:688126) acquired Xinsheng in 2016. At 688126's April 2020 IPO Sinyang held 7.51%; it has sold down to 110,455,692 shares (~4.0%) as of Sept 30, 2025, including a ~14m-share sale in H2 2025 to fund capex. Crucially, the stake is classified as FVOCI ("其他权益工具投资"), so mark-to-market swings (a ~RMB 707m gain sat in Other Comprehensive Income in the 2025 Q3 accounts) flow to equity, not net profit. The P&L fair-value line was only RMB 0.292m in 2024. The distortion is therefore mostly to the gap between headline and recurring profit (2022 net −43% on fair-value losses; 2023 +213% on the reversal) and to book equity; not to operating earnings in recent years.

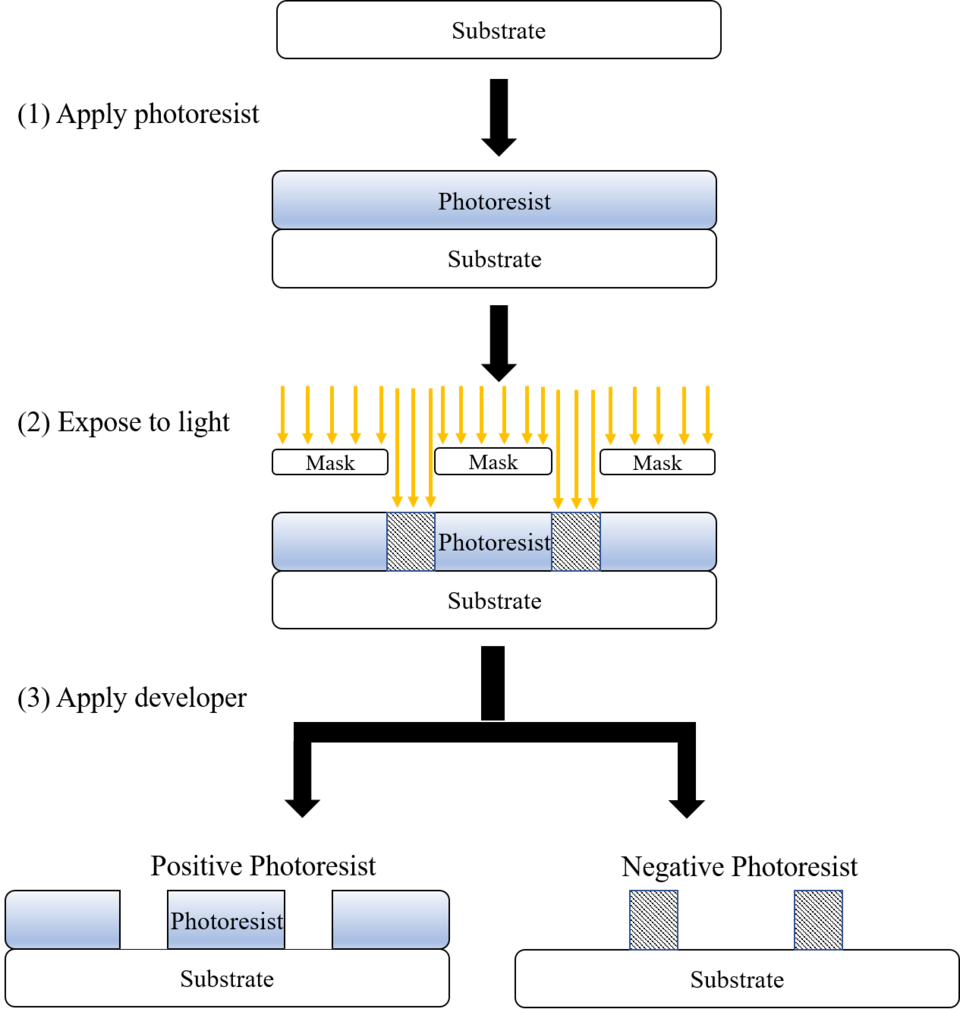

4. Photoresist: three layers must be distinguished.

- Reported qualification milestones: KrF (248nm) thick-film photoresist passed customer verification and won its first order on June 30, 2021, reaching stable mass production in 2022; multiple KrF products are now in batch sale. I-line and KrF have been sampled at >10 customers, some with small continuous orders. ArF dry-line photoresist's production line is running but the product remains in customer certification. ArF immersion photoresist obtained its first sales order in 2024, described by management as "the first step toward industrialization."

- Actual revenue: The photoresist segment grew >100% year-on-year in 2024, but off a very small base and is not separately quantified as a material revenue line; ArF revenue is negligible.

- Aspirational claims: In December 2020 management projected KrF mass production in 2022 and ArF-dry mass production in 2023, with combined revenue approaching RMB 200m, a target that slipped. The company owns four lithography tools for development: ASML XT1900Gi (ArF immersion), ASML-1400 (ArF dry), Nikon-205C (KrF), Nikon-i14 (i-line).

- Sinyang is one of a handful of Chinese semiconductor-photoresist players; commentators uniformly treat ArF immersion commercialization as high-difficulty, long-cycle (12–18 month qualification) and high-risk. For context, the nearest domestic ArF leader Nata Opto-electronic (南大光电) won a hundred-ton-class ArF photoresist order from SMIC in May 2025 — the first large-scale commercialization of a domestic high-end photoresist, at reported yield >90% and cost roughly 15% below imports (per Eastmoney, Oct 2, 2025). Sinyang has no equivalent scaled ArF order to date.

5. Analyst/opinion landscape is thin and China-domestic. No global-bank coverage exists. Verifiable mainland coverage includes a Guotai Haitong Securities (国泰海通) Q1-2026 note rating the stock "Overweight" (增持) with a target of RMB 104.25, based on 2026–2028 EPS of RMB 1.39/1.83/2.48 and a 75x 2026 P/E (vs. comparable-company 2026 average of 66.28x). Aggregator (Eastmoney/Securities Star) data indicated that over a trailing 90-day window (as of mid-2026), 4 institutions rated the stockk, 2 "Buy," and 2 "Overweight", with an average target of RMB 104.25. Tianfeng, Ping An and Huaxin have published on the name or the photoresist theme historically. Treat these as sparse and domestically sourced.

6. Valuation and ownership. Back in July 2025 the stock traded around RMB 39 with trailing P/E ~59.22x, static P/E ~70.11x, P/B ~2.70x, and market cap ~RMB 12.3bn, which was a premium to the electronic-chemicals sector average P/E of 56.95x. The shares ran from a 52-week low of RMB 29.44 to RMB 54.08 by Nov 27, 2025, then to ~RMB 98 by May 2026, implying a much higher market cap (~RMB 30bn) and richer multiples. The controlling shareholders are the Wang Fuxiang / Sun Jiangyan / Wang Su family; controlling vehicle Shanghai Xinke Investment cut its stake from 7.31% to 6.67% by selling 2m shares at an average RMB 39.06 on July 1–2, 2025. Top-10 shareholders held 45.65% (2024). Mutual funds held roughly 9.6% of the float. China's National IC Industry Investment Fund ("Big Fund") does not appear as a direct Sinyang shareholder, though it holds peers (Anji 11.57%, Jingrui 4.99%). Sinyang is itself an LP in state-linked funds (聚源启新, 3.75%; 芯链融创, 4.29%).

7. Peer set (all tickers verified).

- Anji Microelectronics Technology (Shanghai) (安集科技) SHA:688019 (STAR Market). CMP slurry and photoresist-remover leader; gross margins 55–58%; Big Fund holds 11.57%. Closest "high-margin functional wet-chemical" comp.

- Jiangsu Nata Opto-electronic Material (南大光电) SZSE:300346. The premier domestic ArF photoresist player (ArF immersion in mass production, 6 products qualified, the ~100-ton SMIC order of May 2025). Closest ArF comparable.

- Jiangsu Jingrui Electronic Materials (formerly Jingrui Shares) (晶瑞电材) SZSE:300655. High-purity wet chemicals + photoresist; FY2025 revenue RMB 1.61bn, net profit RMB 149m (turnaround); photoresist revenue RMB 223m. (This is the company sometimes rendered "Crystal Clear" (晶瑞) in English)

- Red Avenue New Materials Group (彤程新材) SHA:603650. Domestic KrF share leader; ArF revenue +800% in 2025; FY2025 revenue RMB 3.429bn, net profit RMB 563m, electronic-chemicals revenue RMB 986m; pursuing an H-share listing. Closest KrF comparable.

- Adjacent electronic-chemicals names: Yoke Technology (雅克科技, SZSE:002409), Jianghua Micro (江化微, SHA:603078), Dinglong (鼎龙股份, SZSE:300054), Huate Gas (华特气体, SHA:688268).

8. Bull case. Localization/self-sufficiency tailwinds are strong. Per TrendForce (Dec 3, 2025, citing Anue), China "aims to produce 40% of its own resists by 2026; up from a localization rate of around 10% in 2024," while Japan "controls over 70% of the global photoresist market, and a staggering 95% of high-end EUV resists." Our own prior findings on the global photoresist supply have reached similar conclusions.

The Big Fund's Phase III, the National Integrated Circuit Industry Investment Fund, incorporated May 24, 2024 with registered capital of RMB 344bn (~US$47.5bn), its largest tranche, led by the Ministry of Finance, prioritizes core materials including photoresist, and Beijing rolled out its first EUV-photoresist testing standard in October 2025 to set a clearer technical framework. Sinyang is a validated "China chain" supplier; its damascene copper sulfate and dry-etch post-clean chemistries were first qualified on SMIC's S1 line, and it claims to be the only domestic firm covering copper interconnect across all 90–14nm nodes, supplying 56 twelve-inch and 23 eight-inch fab lines. Copper-plating/additive revenue grew >50% in 2024 (advanced-packaging plating +116%); cleaning +47%; TSV fill capability (20:1 aspect ratio) is described as world-leading. Wet-process capacity is expanding (Hefei Xinyang to 43,500 t, RMB 1.05bn; a new RMB 1.85bn 50,000 t/yr project).

9. Bear case. (a) Photoresist commercialization risk: a persistent gap between qualification headlines and revenue: ArF immersion has one order, not scaled production, in contrast to Nata's ~100-ton SMIC order. (b) Valuation premium: high-50s to 70x trailing P/E in 2025 rising further in 2026, ahead of recurring-earnings growth. (c) Earnings quality: the 688126 stake and government subsidies create divergence between headline and recurring profit, and a Shanghai CSRC warning letter was issued in 2022 for an undisclosed disposal of 20,000 688126 shares. (d) Customer concentration is actually low (top-5 = 37.97% in 2024; largest 16.34%), a relative strength, but exposure to the SMIC/Hua Hong fab-capex cycle is high. (e) Dependence on imported precursors/equipment (ASML/Nikon lithography tools; some imported raw materials) and intensifying domestic competition in commodity wet chemicals. No short-seller reports or credit-rating-agency actions were found, typical for a ChiNext small/mid cap.

10. Export-control / subsidy backdrop (2023–2026). Building on July 23, 2023 controls covering 23 equipment categories, Japan's METI on January 31, 2025 revealed proposed amendments to its Foreign Exchange Order / Export Trade Control Order adding tighter restrictions on chip testing and measurement equipment, CAD software, materials and semiconductors (per CSIS translation and DigiTimes). In November 2025, amid Japan–China tensions, unverified claims that "Canon, Nikon and Mitsubishi Chemical have suspended photoresist shipments to China" spread on social media around Nov 18; Asia Times cautions these are "dubious" because Canon and Nikon make lithography machines/parts and Mitsubishi Chemical supplies only Lithomax (a raw material). Commercial Times separately reported that Shin-Etsu Chemical and Tokyo Ohka (together ~80% of the global market) "paused ArF photoresist shipments to certain Chinese fabs," though Tokyo issued no official ban. These reports are unconfirmed by the Japanese government or the named companies and carry material uncertainty; but they sharpen the strategic value of domestic ArF/KrF capability, a direct tailwind to Sinyang's photoresist optionality.

Details

Sinyang's investment case is best understood as two distinct businesses bolted to a legacy financial asset. The operating story (wet-process chemistries for advanced-node and advanced-packaging fabs) is genuinely strong and accelerating: FY2025 semiconductor revenue of RMB 1.517bn (+46.50%) with a 45.88% gross margin, driven by electroplating/additives (+40% in 2025), cleaning and etching. This is not a speculative franchise; it is an entrenched qualified supplier to the Chinese foundry base.

The photoresist narrative, which drives the equity's "theme" premium and its correlation with the volatile A-share "photoresist concept" basket, is far earlier-stage than the headlines imply. KrF thick-film (used in 3D NAND) is a real, if small, product; ArF dry and immersion remain predominantly in multi-year customer certification. Investors paying 60–75x earnings are underwriting an ArF ramp that has, to date, produced one immersion order; while the domestic ArF leader (Nata) has already secured a hundred-ton fab order.

The 688126 stake is the classic "earnings-quality" wrinkle. Because it is FVOCI, it does not inflate operating profit, but it distorts year-on-year net-profit optics (the −43% 2022 / +213% 2023 swing) and inflates book equity, and periodic disposals generate cash (and occasional compliance missteps). Analysts should anchor on recurring (扣非) profit, which grew a healthier but less dramatic ~10% (2023), ~31% (2024) and ~70% (2025).

Recommendations

- Base case: treat as a wet-chemicals compounder with a free photoresist option, not a photoresist pure-play. Underwrite the copper-plating/cleaning/etching franchise on recurring (扣非) earnings; assign only modest value to ArF until scaled revenue appears.

- Stage 1 (next 2 quarters): Confirm the operating trajectory via H1-2026 and Q3-2026 filings — watch semiconductor-segment revenue growth (>30% sustains the thesis) and gross margin (a recovery above 46% signals capacity ramp maturing).

- Stage 2 (photoresist inflection): Upgrade only if the company discloses ArF immersion repeat/volume orders from a named fab (SMIC/Hua Hong) or a separately quantified photoresist revenue line materially above RMB 100m. That is the single datapoint that would justify the theme premium.

- De-rate triggers: trailing P/E sustained above ~70x without recurring-EPS acceleration; a stalled ArF qualification; a sharp foundry-capex downturn; or large controlling-shareholder selling beyond the disclosed 0.64% program.

- Data hygiene: every multiple and target in this file carries an as-of date; the RMB 104.25 target predates any FY2025-final re-rating and should be refreshed against the latest filing before publication.

Source list (Chicago author-date, for a reference list)

- China Securities Journal (中证网). 2020. "沪硅产业科创板上市首日涨180%." April 21. https://www.cs.com.cn/ssgs/gsxw/202004/t20200421_6048054.html

- Cninfo (巨潮资讯). 2025. "上海新阳半导体材料股份有限公司2024年年度报告." April 18. https://static.cninfo.com.cn/finalpage/2025-04-18/1223141520.pdf

- Cninfo (巨潮资讯). 2024. "天风证券关于上海新阳变更部分募集资金用途、调整项目实施进展及部分募投项目结项的核查意见." March 15. http://static.cninfo.com.cn/finalpage/2024-03-15/1219307300.PDF

- Dongfang Caifu / Eastmoney (东方财富). 2024. "上海新阳半导体材料股份有限公司公告 (2024-010, 高端光刻胶项目)." March 14. https://pdf.dfcfw.com/pdf/H2_AN202403141626764456_1.pdf

- Dongfang Caifu / Eastmoney (东方财富). 2026. "上海新阳投资者关系活动记录表." May 12. https://pdf.dfcfw.com/pdf/H2_AN202605121822223684_1.pdf

- Eastmoney (东方财富). 2025. "南大光电斩获中芯国际ArF光刻胶百吨级订单." October 2.

- Fxbaogao (发现报告). 2026. "国泰海通证券:上海新阳2026年一季报点评 (增持, 目标价104.25元)." https://www.fxbaogao.com/detail/5390880

- Jiemian News (界面新闻). 2025. "上海新阳(300236.SZ):2024年年报净利润为1.76亿元." April 18. https://www.jiemian.com/article/12630259.html

- Jiemian News (界面新闻). 2024. "上海新阳(300236.SZ):2024年中报净利润为5890.41万元." August 19. https://www.jiemian.com/article/11574318.html

- Sina Finance (新浪财经). 2026. "上海新阳2025年报解读:净利增71.12% 经营现金流翻倍至4.75亿元." March 12. https://finance.sina.com.cn/stock/aigc/stockfs/2026-03-12/doc-inhqtusm4701060.shtml

- Sina Finance (新浪财经). 2026. "上海新阳2025年度业绩预告:净利润同比增长50.82%-82.12%." January 23. https://finance.sina.com.cn/tech/roll/2026-01-23/doc-inhiicfs1913306.shtml

- Sina Finance (新浪财经). 2025. "上海新阳预计2025年营收超17亿." September 12. https://finance.sina.com.cn/roll/2025-09-12/doc-infqerft7862296.shtml

- Sina Finance (新浪财经). 2024. "沪硅产业:2023年净利润同比下降42.61%." April 13. https://finance.sina.com.cn/roll/2024-04-13/doc-inarsfvu6975225.shtml

- Sina (mirror of SZSE filing). 2025. "上海新阳半导体材料股份有限公司2024年年度报告全文." April 18. http://file.finance.sina.com.cn/211.154.219.97:9494/MRGG/CNSESZ_STOCK/2025/2025-4/2025-04-18/10895370.PDF

- Cninfo. 2025. "上海新阳2024年年度报告 (前五大客户/供应商)." April 18. https://static.cninfo.com.cn/finalpage/2025-04-18/1223141520.pdf

- Sohu (搜狐, from Sinyang 2024 annual report). 2025. "上海新阳2024年年报解读." https://www.sohu.com/a/886143871_122014422

- Cailian Press (财联社/CLS). 2021. "下游晶圆厂加速验证 上海新阳首获光刻胶订单." June 30. https://www.cls.cn/detail/780744

- Cailian Press (财联社/CLS). 2023. "上海新阳:ArF光刻胶在客户端验证中." September 12. https://www.cls.cn/detail/1797399

- Laoyaoba / Jiwei (集微). 2026. "【2025年报快解】上海新阳:归母净利增长71.12%." March 13. https://jiweipreview.laoyaoba.com/n/991170

- Securities Times (证券时报/STCN). 2025. "上海新阳一季度净利同比增长171% 拟投资18.5亿元扩大产能." https://www.stcn.com/article/detail/1673528.html

- Securities Times (证券时报/STCN). 2022. "上海新阳违规减持遭警示." https://www.stcn.com/article/detail/1151745.html

- Xinhua (新华网). 2025. "上海新阳控股股东计划减持0.64%股份." May 13. http://www.news.cn/finance/20250513/959288b5ef3b42579d2e2edbb1bdc726/c.html

- Sina Finance (新浪财经). 2025. "上海新阳:控股股东上海新科减持200万股,减持计划完成." July 3. https://finance.sina.com.cn/stock/aigc/zjchg/2025-07-03/doc-infeezvi3861902.shtml

- NetEase (网易/163). 2025. "上海新阳收盘下跌1.08%,滚动市盈率59.22倍,总市值123.19亿元 (行业估值对比表)." https://c.m.163.com/news/a/K50PRQUH0519QIKK.html

- Stockstar (证券之星). 2026. "上海新阳(300236)5月15日主力资金净卖出... (机构评级/目标价104.25)." May 18. https://stock.stockstar.com/RB2026051800003028.shtml

- Stockstar (证券之星). 2026. "上海新阳:2026年一季度报告." April 29. https://stock.stockstar.com/notice/SN2026042900010738.shtml

- Stockstar (证券之星). 2025. "沪硅产业:中金公司关于本次重组前发生业绩异常之专项核查意见." May 20. https://stock.stockstar.com/notice/SN2025052000031920.shtml

- 21st Century Business Herald (21经济网). 2025. "沪硅产业收购预案出炉,将全资控股'新昇系'." March 8. https://www.21jingji.com/article/20250308/herald/d57ac1edcb87f9830d7a7b2e22518589.html

- Ministry of Science and Technology (科技部). 2015. "'40-28纳米集成电路制造用300毫米硅片'项目在沪启动." August 24. https://www.most.gov.cn/dfkj/sh/zxdt/201508/t20150824_121267.html

- SZSE / Longan Law Firm (北京市隆安律师事务所). 2020. "关于上海新阳2020年度向特定对象发行股票的补充法律意见书(一)." December 14. https://disc.static.szse.cn/disc/disk02/finalpage/2020-12-14/b53a39e7-01ad-458a-ac86-196244b4767a.PDF

- Sina Finance (新浪财经). 2022. "不止晶圆代工,中芯国际捧出10个IPO." June 20. https://finance.sina.cn/china/gncj/2022-06-20/detail-imizmscu7842692.d.html

- Zhihu / 前瞻 (Qianzhan). 2021. "2021年中国光刻胶行业上市公司全方位对比." https://finance.sina.com.cn/roll/2021-10-08/doc-iktzqtyu0200944.shtml

- Xueqiu (雪球). 2026. "彤程新材(SH603650)公司概况." https://xueqiu.com/S/SH603650

- Investing.com. 2025. "Red Avenue New Materials Group (SS:603650) stock overview." November 23. https://www.investing.com/equities/red-avenue-new-materials-group

- TrendForce. 2025. "Japan Rumored to Curb Photoresist Exports as China Targets 40% Self-Sufficiency by 2026." December 3. https://www.trendforce.com/news/2025/12/03/news-japan-rumored-to-curb-photoresist-exports-as-china-targets-40-self-sufficiency-by-2026/

- Asia Times. 2025. "Rumored Japan photoresist ban sparks China's worst fears." November. https://asiatimes.com/2025/11/rumored-japan-photoresist-ban-sparks-chinas-worst-fears/

- CSIS. 2025. "CSIS Translation: January 2025 Updated Japanese Export Controls on High-Performance Semiconductor Manufacturing Equipment." https://www.csis.org/analysis/csis-translation-january-2025-updated-japanese-export-controls-high-performance

- DigiTimes. 2026. "China expedites photoresist localization to reduce Japan reliance." January 15. https://www.digitimes.com/news/a20260115PD221/

- Crunchbase. 2025. "Shanghai Sinyang Semiconductor Materials — company profile (founded Jul 1 1999; IPO Jun 29 2011; SZSE:300236)." https://www.crunchbase.com/organization/shanghai-sinyang-semiconductor-materials

- Sinyang official site (English). http://en.sinyang.com.cn/