Samarium-Cobalt vs Neodymium Magnets (SmCo vs NdFeB): Performance, Cost, and Aerospace Applications

NdFeB offers double the energy product at lower cost; SmCo holds performance to 350°C. When to choose each for aerospace and high-temp design.

TL;DR

- NdFeB wins on raw performance and price-per-joule; Sm₂Co₁₇ wins on heat, stability, and corrosion. NdFeB delivers roughly double the energy product (up to ~52 MGOe vs. ~24–32 MGOe for SmCo) at typically one-half to one-third the finished cost per kilogram, but loses magnetism rapidly above ~80–150°C, while Sm₂Co₁₇ holds performance to 300–350°C with temperature coefficients three to four times smaller, making it the default for aerospace, defense, and high-temperature designs.

- The supply chain for both is a Chinese bottleneck, and the April 4, 2025 export controls (MOFCOM Announcement No. 18) specifically named samarium, dysprosium, and terbium; these remain fully in force as of mid-2026 (only the broader October 2025 expansion was suspended to November 2026), directly hitting SmCo (which is wholly controlled) and high-coercivity NdFeB (which needs controlled Dy/Tb), with defense/aerospace end-uses explicitly excluded from general licenses.

- The strategic action is reshoring: the DoD–MP Materials partnership (announced July 10, 2025) sets a 10-year $110/kg NdPr price floor and funds expansion from 3,000 to 10,000 t/yr of magnet capacity (the "10X Facility," commissioning expected 2028), while Permag/Electron Energy Corporation remains the only U.S. SmCo producer; treat SmCo as a small, defense-critical niche and NdFeB as the volume battleground.

SmCo vs NdFeB Magnets: High-Temperature Performance, Cost, and Aerospace Trade-offs

Key Findings

1. Intrinsic properties cleanly separate the two materials by mission. NdFeB offers the highest commercial remanence (Br up to ~1.43 T / 14.3 kGauss for N52) and energy product (up to ~52–55 MGOe), but a low Curie temperature (~310–400°C) and large reversible temperature coefficients (αBr ≈ −0.09 to −0.12 %/°C; βHcj ≈ −0.40 to −0.62 %/°C). Sm₂Co₁₇ trades energy density (Br ~1.0–1.12 T, BHmax ~24–32 MGOe) for a Curie temperature near 800–850°C, max operating temperatures of 300–350°C, and far smaller coefficients (αBr ≈ −0.030 to −0.035 %/°C; βHcj ≈ −0.20 %/°C).

2. Corrosion and coating economics favor SmCo in harsh environments. NdFeB's high iron content makes it corrosion-prone, requiring Ni/Cu/Ni, zinc, or epoxy coatings; SmCo is inherently corrosion-resistant and is frequently used uncoated. Both are brittle sintered ceramics susceptible to chipping and vibration fracture.

3. SmCo costs 2–3× more per kg, driven by cobalt and low production volume. Finished sintered NdFeB runs roughly $65–120/kg for mid-grades (with high-coercivity SH/UH grades reaching $130–175/kg), while finished Sm₂Co₁₇ runs roughly $150–300/kg. Cobalt (~50% of Sm₂Co₁₇ by weight) is the dominant and most volatile cost driver; cobalt metal roughly doubled over 2025, entering 2026 at US$56,414/tonne (~$25/lb), highs not seen since July 2022 after the DRC export ban/quota.

4. China controls the majority of both chemistries; export controls have weaponized this. China accounted for 94% of permanent-magnet production and 91% of refined rare-earth output in 2024 (IEA). The April 2025 controls placed samarium, dysprosium, terbium, and four other elements under MOFCOM licensing, capturing all SmCo magnets and any Dy/Tb-bearing NdFeB.

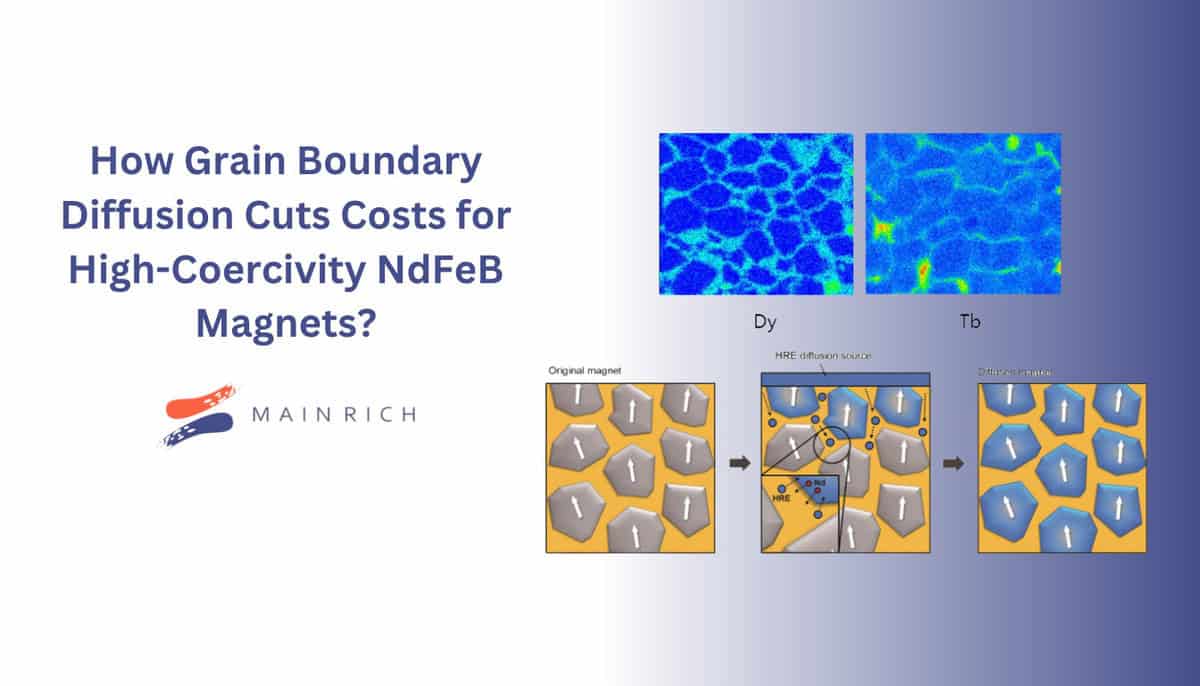

5. Mitigation is advancing on two fronts: thrift and substitution. Grain boundary diffusion (GBD) cuts Dy/Tb usage by concentrating it at grain boundaries; rare-earth-free iron nitride (Niron Magnetics, Fe₁₆N₂) and reshored capacity (MP Materials, Permag/EEC) are scaling but remain years from displacing Chinese volume.

Details

Magnetic and physical properties by grade

NdFeB (sintered). Standard grades scale from N27 (Br 1.03 T, BHmax ~199 kJ/m³ / 25 MGOe) through N52 (Br 1.43 T, BHmax ~382–414 kJ/m³ / 48–52 MGOe), with N55 the strongest routinely produced grade at ~51–55 MGOe. Intrinsic coercivity (Hcj) of standard grades is ~955 kA/m (12 kOe); the coercivity suffix grades raise this substantially: SH grades guarantee Hcj ≥ ~1592 kA/m (20 kOe), and UH grades ≥ ~1990 kA/m (25 kOe).

These suffixes set maximum operating temperature: no suffix ≤80°C (N52/N55 only ~60°C), M ≤100°C, H ≤120°C, SH ≤150°C, UH ≤180°C, EH ~200°C, AH ~220–230°C.

The Curie temperature is ~310–400°C. Arnold Magnetics' N52 datasheet lists αBr = −0.12 %/°C and βHcj = −0.62 %/°C (20–100°C). N48SH measured values: Br 13.82 kGs at 20°C falling to 11.69 kGs at 150°C; Hcj collapsing from 21.06 kOe to 6.29 kOe over the same range (α ≈ −0.119 %/°C, β ≈ −0.539 %/°C).

Sm₂Co₁₇ (2:17, sintered). Typical grades (per Eclipse Magnetics, Integrated Magnetics, thyssenkrupp datasheets) span Br ~1.0–1.12 T (10.0–11.2 kGauss), Hcj from ~400 kA/m (low-coercivity variants) up to ~1990 kA/m (25 kOe), and BHmax ~24–32 MGOe (190–240 kJ/m³).

Arnold's RECOMA 35E is marketed as the highest-energy SmCo grade. Maximum operating temperature is typically 300–350°C, with ultra-high-temperature (UHT) grades claimed to operate at 400–550°C in space applications.

The Curie temperature is ~800–850°C. Reversible coefficients are roughly αBr = −0.030 to −0.035 %/°C and βHcj = −0.20 %/°C - i.e., NdFeB's flux loss with temperature is 3–4× larger than SmCo's. The original SmCo₅ (1:5) grade has even better corrosion resistance (contains no iron) but lower energy product.

The practical implication:

NdFeB's room-temperature advantage erodes with heat. SmCo magnets outperform NdFeB above roughly +150 to +180°C, and remain functional where NdFeB would irreversibly demagnetize.

Why properties map to aerospace and high-temperature regimes

Permanent-magnet synchronous machines (PMSMs) for "more-electric aircraft" overwhelmingly favor SmCo because of robustness in harsh thermal environments and lower demagnetization risk; peer-reviewed reviews note NdFeB's Br and Hcj reductions are 3–4× greater than SmCo's at elevated temperature. Specific aerospace/defense uses for SmCo include: missile guidance and fin actuators (low αBr/βHcj Sm₂Co₁₇ with Cu/Zr cell-boundary pinning); satellite reaction wheels, momentum/bias wheels, and magnetic bearings (proven heritage including DSP-satellite-derived magnetically suspended reaction wheels and EEC magnets aboard NASA's Deep Space 1 ion engine); jet-engine sensors and avionics in hot gas paths; traveling-wave-tube magnet stacks for radar; gyroscopes and inertial guidance; and high-temperature downhole tools. Integrated Power Units in the MEA initiative target magnetic materials operating above 400°C, which is beyond NdFeB's reach entirely.

NdFeB dominates where temperatures are moderate and energy density per unit volume/weight is paramount: EV traction motors (typically 1.5–3.0 kg of NdFeB per vehicle, with heavy rare earths added for 150–200°C winding temperatures), direct-drive wind turbine generators, consumer electronics, hard disk drives, robotics, and power tools.

Cost and supply structure

Rare-earth feedstock (2025–2026). The market bifurcated sharply after April 2025: Chinese domestic NdPr sat near $60/kg while ex-China prices surged. Retail/investor benchmarks (Strategic Metals Invest) listed neodymium at ~$244.90/kg and praseodymium at ~$245.40/kg in mid-June 2026; dysprosium ~$930.70/kg and terbium oxide ~$985/kg. Samarium oxide, historically cheap and stable (~$49/kg in 2024, projected ~$58/kg in 2026 by some trackers), saw FOB Shanghai prices firm through 2025 under quota and export-control pressure.

Cobalt and the SmCo cost structure. Sm₂Co₁₇ is ~50% cobalt and ~25% samarium by weight (balance Fe, Cu, Zr). Cobalt is the dominant and most volatile cost driver. The DRC supplies ~70–76% of mined cobalt; China leads refined cobalt. The DRC imposed a total export ban on February 22, 2025, extended it in June, then replaced it with a restrictive quota effective October 2025: 96,600 t/yr for 2026–2027 (with ARECOMS retaining a 10%/~9,660 t reserve, leaving ~86,940 t allocable; CMOC's 2026 quota ~31,200 t and Glencore's combined ~22,800 t), roughly half of 2024 export levels. Cobalt prices more than doubled across 2025, entering 2026 at US$56,414/tonne (~$25/lb).

Finished-magnet pricing. Sintered NdFeB: ~$65–120/kg mid-grade, $130–175/kg for high-coercivity SH/UH grades; an N52 costs ~20–40% more than an N35 of equal size, and an SH grade ~60% more than the base grade due to Dy/Tb additions. Sintered Sm₂Co₁₇: ~$150–300/kg, with high-cobalt custom grades at the top of that range. The SmCo premium reflects cobalt cost, longer/more complex heat treatment, and far smaller production volumes.

Heavy rare earths and grain boundary diffusion. Dy and Tb raise NdFeB coercivity and Curie temperature but reduce Br/BHmax via antiferromagnetic coupling, and are expensive and supply-constrained. GBD concentrates Dy/Tb at grain boundaries (where they most effectively block reverse-domain nucleation), achieving the same temperature class with up to ~70% less heavy rare earth. A 2026 study (Shanxi Normal University et al., Rare Metals) reported synergistic Dy/Tb dual-layer diffusion lifting coercivity from 12.56 to 22.66 kOe (~80%) while preserving energy density. Bunting/Magnet Applications notes peak NdFeB grades that were 2–4% Dy in 2014 are now Dy-free at the same performance.

Current state of the field

Producers. China hosts the largest sintered NdFeB makers — JL MAG Rare-Earth (SHE:300748), Beijing Zhong Ke San Huan, Ningbo Yunsheng, Yantai Zhenghai (SHE:300224), Innuovo Magnetics, Earth-Panda — and controls the dominant share of output. Japan's leaders are Proterial (formerly Hitachi Metals, NEOMAX brand), Shin-Etsu Chemical (TYO:4063), and TDK (TYO:6762). Germany's VACUUMSCHMELZE (VAC) integrates basic elements to finished motor stators and signed a GM supply deal. Western/specialist players include Arnold Magnetic Technologies (RECOMA SmCo), Electron Energy Corporation (the only U.S. SmCo producer, now part of Permag alongside Dexter and MCE), Noveon Magnetics (recycled NdFeB), MP Materials (NYSE:MP), USA Rare Earth (NSYE:USAR), and Niron Magnetics (rare-earth-free). Permag

Geographic concentration and risk. China mines roughly 60% of rare earths, processes ~91% of refined output, and made 94% of permanent magnets in 2024 (IEA). The U.S. was ~67% net-import-reliant for REEs in 2025 and lacks heavy-rare-earth separation at scale — the processing gap is more binding than the mining gap.

Substitution. Niron Magnetics' iron nitride (α″-Fe₁₆N₂) "Clean Earth Magnet" claims magnetization ~18% above NdFeB but is limited to ~150–200°C and faces phase-stability and coercivity challenges. Niron broke ground on September 26, 2025 on a $169.7M, 190,000-sq-ft, 1,500-ton/yr plant in Sartell, Minnesota (operational targeted early 2027), and lists Stellantis, Samsung, Allison Transmission, and Magna among partners sampling from its 2024 Minneapolis pilot plant (a Stellantis collaboration on rare-earth-free motors was announced October 16, 2025). Tetrataenite (L1₀-FeNi) and recycling are also being pursued but are not yet at commercial scale.

Export controls (status mid-2026). MOFCOM Announcement No. 18 (April 4, 2025) placed samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium — plus their oxides, alloys (explicitly including samarium-cobalt), and downstream magnets — under per-shipment export licensing. All SmCo magnets and any Dy/Tb-bearing NdFeB are captured; NdFeB made only from light rare earths (Nd, Pr, La, Ce) remains freely exportable. This April regime was never suspended. The October 9, 2025 escalation (adding five elements plus an extraterritorial FDPR-style 0.1% rule) was suspended for one year — to roughly November 2026 — under the Trump–Xi Busan/Beijing détente. General licenses issued from December 2025 (to JL MAG, Zhong Ke San Huan, Yunsheng) eased civilian throughput, but defense and aerospace end-uses remain explicitly off-limits, and applications tied to foreign military programs are automatically rejected.

Reshoring. The DoD–MP Materials partnership (announced July 10, 2025; per MP's SEC 8-K/press release) includes a $400M DoD Series A convertible preferred equity stake, a 10-year $110/kg NdPr price floor (vs. MP's 2024 realized ~$51/kg, per the Payne Institute at Colorado School of Mines), a 10-year offtake for 100% of the new "10X" facility's output, and a $150M loan for heavy-rare-earth separation — scaling MP from 3,000 to 10,000 t/yr of magnet capacity, with the 10X Facility commissioning expected in 2028. Permag/EEC announced a multi-million-dollar expansion more than doubling U.S. SmCo capacity (August 2025) and DFARS 252.225-7052 compliance by mid-2026, ahead of the January 1, 2027 mandate.

Recommendations

For aerospace/defense OEMs and program managers (act now):

- Default to Sm₂Co₁₇ for any magnet seeing >150°C, thermal cycling, radiation, or corrosive environments (engine sensors, actuators, reaction wheels, magnetic bearings, TWTs). Qualify a DFARS-compliant domestic source — realistically Permag/EEC or Arnold — before the January 2027 DFARS deadline, and assume Chinese SmCo is unavailable for defense end-use given the April 2025 controls.

- Dual-source and stockpile samarium-cobalt finished magnets and feedstock now; samarium and SmCo alloys are under license with no statutory approval deadline and automatic rejection for military end-use.

For EV, wind, and industrial motor designers:

- Stay on NdFeB for volume traction/generator applications but design to the lowest heavy-rare-earth content feasible: specify GBD grades to cut Dy/Tb, and engineer the magnetic circuit (higher permeance coefficient, better cooling) to allow a lower coercivity grade.

- Monitor whether ex-China NdPr settles toward the $110/kg MP floor; below ~$80/kg ex-China, Western supply economics weaken and reshoring timelines slip.

For investors and corporate strategists:

- Treat SmCo as high-margin, defense-anchored niche (small TAM, captive DFARS demand) rather than a volume growth story; the investable scale is in NdFeB and its supply-chain reshoring.

- Watch three thresholds that would change the thesis: (1) the November 2026 expiry/renewal of the October 2025 control suspension; non-renewal would re-impose extraterritorial FDPR-style rules; (2) cobalt sustaining above ~$25/lb, which directly inflates SmCo cost; and (3) Niron Fe₁₆N₂ reaching automotive-qualified volume (its Stellantis/Magna/Allison engagements are the signal to track), which would pressure low-coercivity NdFeB demand.

Caveats

- Finished-magnet $/kg figures are trade-level estimates, not exchange data. Tier-1 price-reporting agencies (Adamas Intelligence, Project Blue, Fastmarkets, IDTechEx, Benchmark) publish finished-magnet pricing only behind paywalls; the $/kg ranges here come from manufacturer and trade sources and vary with size, shape, coating, grade, and order volume.

- Rare-earth element price benchmarks diverge widely. Retail/investor quotes (e.g., neodymium ~$245/kg) differ greatly from Chinese domestic NdPr (~$60/kg) and from oxide-vs-metal benchmarks; the post-April-2025 ex-China/in-China bifurcation makes a single "price" misleading. Figures should be cross-checked against a consistent benchmark before financial use.

- SmCo composition figures conflict in secondary sources. The values are ~50% cobalt and ~25% samarium by weight for Sm₂Co₁₇; some trade sources cite 33–37% samarium or an erroneous 12–14% cobalt.

- Some market-size, demand-forecast, and "by 2026/2028" figures are projections subject to revision; they are presented as forecasts, not realized data. Maximum-temperature claims of 500–550°C for SmCo apply to specialized UHT grades and specific permeance-coefficient conditions, not general 2:17 product.