Sodium-Ion Batteries in 2026: Cost Reality vs. LFP, CATL's Naxtra, and the Hard Carbon Bottleneck

China holds 95%+ of sodium-ion capacity. CATL's Naxtra hits 175 Wh/kg. Yet at 2026 prices, SIB cells still cost more than LFP.

Summary

Sodium-ion batteries (SIBs) have crossed from laboratory curiosity to genuine commercial reality in 2026, but their competitive envelope is narrow and application-specific rather than disruptive. The single most important finding of this report: SIBs are now a credible, deployable technology for cost- and safety-sensitive niches (stationary storage, entry-level and urban EVs, two- and three-wheelers, cold-climate applications, and industrial backup), yet they do not threaten lithium-ion's dominance in mainstream long-range EVs, and their much-touted cost advantage over lithium iron phosphate (LFP) has not materialized at 2025-2026 lithium prices. The following findings carry the confidence levels noted.

SIB cell energy density has reached ~175 Wh/kg in mass production (CATL Naxtra), closing much of the gap to LFP's ~200-205 Wh/kg, but volumetric density remains materially inferior (17-49% lower in modeled current designs).

The cost advantage over LFP is contingent, not structural: at lithium carbonate prices near $10,000/tonne LCE, virtually no SIB roadmap undercuts LFP absent a graphite supply disruption; sustained prices near $50,000/tonne would tip more than 55% of SIB roadmaps to a durable price advantage before 2035 [4].

China holds an overwhelming and durable lead: more than 95% of installed and announced SIB manufacturing capacity, the dominant patent position, and the only mass-production passenger EV (Changan Nevo A06, CATL Naxtra, mid-2026) [1][9][13].

Western efforts are fragile: Natron Energy, the US commercial pioneer, ceased operations in September 2025; survivors (Peak Energy, Altris, Tiamat) are early-stage and focused on stationary storage, not EVs [15].

The supply-chain resilience argument is partial: SIBs eliminate lithium, cobalt, and nickel, but the hard carbon anode supply chain is immature and concentrated in China, and cathode chemistries reintroduce dependencies (vanadium in NVPF) [1][25].

Sodium-Ion Batteries: Technology, Markets, and Strategic Position in a Lithium-Focused World

1. Context and Scientific Foundations

1.1 Working principle and the sodium penalty

Sodium-ion batteries operate on the same "rocking chair" intercalation principle as lithium-ion batteries (LIBs), shuttling Na⁺ ions between cathode and anode through a liquid electrolyte. The appeal is elemental: sodium is roughly 1,000 times more abundant in the Earth's crust than lithium and about 60,000 times more plentiful in the oceans, and sodium carbonate traded at $100-500/tonne over 2020-2024 versus $6,000-83,000/tonne for lithium carbonate. [3]

The chemistry, however, imposes intrinsic penalties. Sodium's larger ionic radius (1.02 Å vs. 0.76 Å for lithium), higher molar mass (23.0 vs. 6.9 g/mol), and less negative standard electrode potential (-2.71 V vs. -3.02 V) all reduce achievable energy density. Critically, sodium does not appreciably intercalate into graphite because binary sodium-graphite intercalation compounds are thermodynamically unstable. This single fact forces SIBs onto hard carbon anodes rather than the mature, cheap graphite of the LIB industry, and hard carbon is the principal bottleneck to higher SIB energy density. [5]

1.2 The structural advantage: aluminum on both electrodes

Because sodium does not alloy with aluminum at low potential (unlike lithium, which forms LiAl, Li₃Al₂ and similar alloys), SIBs can use aluminum current collectors on both electrodes, eliminating the copper foil required on LIB anodes. This delivers three benefits: modest cost and weight reduction; and, most importantly, true zero-volt transport and storage. When a cell is discharged to 0 V, the copper collector in a LIB oxidizes and dissolves, risking internal shorts and dendrites; aluminum resists this oxidation. SIBs can therefore be shipped and stored fully de-energized, sharply reducing fire risk in transport and enabling safer battery swapping. This is a demonstrated, peer-reviewed advantage, not a marketing claim, and it is unavailable to conventional LIBs. [5][26]

1.3 Cathode chemistry families

Three cathode families dominate, each with a distinct performance and cost profile:

- Layered transition-metal oxides (NaxTMO₂, TM = Ni, Mn, Fe, Cu, Ti). Highest energy density (theoretical capacities 200-240 mAh/g), favored where energy density matters most. CATL's Naxtra and HiNa's early cells follow this path. Drawbacks: air/moisture sensitivity (surface carbonate formation), the shortest cycle life of the three families, and the greatest propensity to thermal runaway. [5]

- Polyanionic compounds (NVPF: Na₃V₂(PO₄)₂F₃; NFPP: Na₄Fe₃(PO₄)₂(P₂O₇)). Strong P-O covalent bonds resist oxygen release above 300°C, giving excellent thermal stability and cycle life; higher average discharge voltage (~3.85 V for NVPF). Used by Tiamat (NVPF) and Peak Energy (NFPP). Drawback: NVPF depends on vanadium, and production of these materials is almost exclusively Chinese. [5][18]

- Prussian blue analogues (PBAs) and Prussian white. Very low material cost (iron- and manganese-based), long cycle life, and the "zero-strain" framework prized for high cycle counts. Used by Natron (PBA) and Altris/Faradion (Prussian white). Drawback: lower volumetric density and moisture sensitivity in some formulations. [15][19]

Independent modeling published in Energy & Environmental Science (2025) benchmarked all three families at gigafactory scale against a graphite/LFP pouch reference (214 Wh/kg, 507 Wh/L): layered oxide SIB cells reached 147-206 Wh/kg (333-419 Wh/L), polyanionic 158-192 Wh/kg (310-366 Wh/L), and PBA 161-185 Wh/kg (260-302 Wh/L). The study's central conclusion is that the energy gap is driven primarily by the inferior capacity, voltage, and density of hard carbon relative to graphite, and that optimized hard carbon (375 mAh/g target) could narrow or close the gravimetric gap for selected chemistries. [5]

1.4 Performance envelope versus LFP and NMC benchmarks

| Metric | SIB (production 2025-26) | LFP | NMC |

|---|---|---|---|

| Gravimetric energy density (cell) | 140-175 Wh/kg (CATL Naxtra 175 | 180-205 Wh/kg | 240-280 Wh/kg |

| Volumetric energy density (cell) | ~260-420 Wh/L | ~500 Wh/L | 500-700 Wh/L |

| Nominal cell voltage | 3.0-3.3 V | 3.2 V | 3.6-3.7 V |

| Cycle life | 2,000-10,000+ (chemistry-dependent) | 3,000-6,000 | 1,000-2,000 |

| Low-temperature performance | ~90% capacity at -20°C to -40°C | ~70-85% at -20°C | Poor below -10°C |

| Zero-volt transport | Yes (structural) | No | No |

| Aluminum on both electrodes | Yes | No | No |

The low-temperature performance is a repeatedly demonstrated SIB advantage. CATL claims the Naxtra retains 90% usable capacity at -40°C; the IEA independently confirms SIBs exhibit significantly better cold-weather performance than LFP. The Datang Hubei grid installation's project manager reported 85% charge/discharge efficiency at -20°C in the field. This makes SIBs particularly attractive for northern China, and CATL is deliberately siting over 600 of its planned 3,000+ battery-swap stations in colder northern regions. [1][12][14]

Two important caveats on the headline numbers. First, manufacturer-announced figures (CATL's 175 Wh/kg, ">10,000 cycles," 90% capacity at -40°C) arent independently verified; the third-party GB 38031-2025 safety certification is verified, but the performance specifications are not independently confirmed. Second, the widely repeated "175 Wh/kg matches LFP" framing overstates parity: the IEA puts the latest LFP at up to 205 Wh/kg and notes the SIB disadvantage is greater in volumetric terms, translating to roughly 350 km of real range for an SUV-class SIB pack versus 400-600 km for lithium-ion. [2][12]

2. Applications: Where SIBs Fit, and Where They Do Not

2.1 Competitive today

- Stationary grid storage. The strongest present-day fit. Weight and volume matter little; cycle life, safety, cold-weather tolerance, and lifetime cost dominate. The Datang Hubei plant in Qianjiang (50 MW/100 MWh phase one, world's largest operating SIB storage system, HiNa 185 Ah cells, commissioned June 2024) is the flagship proof point, with a 100 MW/200 MWh full build. Peak Energy in the US has staked its entire business on this thesis with a passively cooled NFPP system. [14][16]

- Two- and three-wheelers and micro-EVs. BYD's 30 GWh Xuzhou plant (with Huaihai) is explicitly targeted at micro-vehicles and scooters, the segment where SIB economics and safety are most compelling and range demands are modest. [20]

- Data center and telecom backup / industrial power. High-power, safety-critical, weight-insensitive. This was Natron's target market (before its collapse) and remains a live segment for Peak/Energy Vault deployments. [15][16]

- Cold-climate applications. A cross-cutting advantage rather than a segment per se. [1]

2.2 Plausibly competitive on announced roadmaps

- Entry-level and urban EVs. The Changan Nevo A06 (45 kWh Naxtra pack, >400 km CLTC, mid-2026) is the test case. JAC's Yiwei/Sehol models (HiNa cells, 23.2 kWh, ~230 km) proved viability but at low volume. Competitive if lithium prices stay elevated and hard carbon scales. [13]

- Hybrid / dual-chemistry packs. CATL's Freevoy dual-power architecture and the IEA both highlight pairing SIB with lithium-ion cells to buy cold-weather resilience. A pragmatic near-term adoption vector. [1][12]

- Starter/SLI and lead-acid replacement. Faradion's founder Jerry Barker argues SIB's best opportunity is displacing lead-acid in combustion vehicles and grid backup. CATL's 24V heavy-truck start-stop Naxtra product targets exactly this, claiming 61% lower lifecycle cost than lead-acid. [12][24]

2.3 Where the physics makes competitiveness unlikely

Long-range passenger EVs, performance vehicles, and any weight- or volume-constrained application (aviation, premium EVs) remain the domain of high-nickel NMC and, increasingly, high-density LFP. The volumetric penalty is the binding constraint, and no announced SIB roadmap closes it against NMC. [2][5]

3. Key Players and Stakeholders

3.1 Chinese incumbents

- CATL (SHE:300750; HKEX:3750). The decisive actor. Launched its Naxtra brand in April 2025, claims 175 Wh/kg and mass production, and became the first to pass China's GB 38031-2025 traction-battery safety standard. With Changan (SHE:000625) it unveiled the Changan Nevo A06, billed as the world's first mass-production sodium-ion passenger vehicle, for mid-2026 delivery. Cumulative sodium R&D investment approached CN¥10bn by end-2025, and CATL announced a further CN¥5bn (~US$735m) for 40 GWh of new sodium capacity in Fujian. Naxtra will be supplied across Changan's Avatr, Deepal, Qiyuan/Nevo and Uni brands. [12][13]

- BYD (SHE:002594; HKEX:1211). Broke ground January 2024 on a 30 GWh sodium plant in Xuzhou with electric two-/three-wheeler maker Huaihai (CN¥10bn / ~US$1.4bn), the world's largest announced SIB plant, targeting micro-vehicles and scooters. Advancing a third-generation sodium platform and separately a sulfide solid-state program. [20] Publicnow

- HiNa Battery (Zhongke Haina). CAS Institute of Physics spin-off (2017), the technology pioneer. Supplied the first production SIB EV (JAC Yiwei, January 2024) and the Datang Hubei grid system. Its Fuyang plant (with China Three Gorges) began at 1 GWh toward a 5 GWh plan. GM Li Shujun projects sodium reaching cost parity with lithium around 2027. [14][21] CnEVPost

- Others. EVE Energy, Huawei (grid systems), and a wave of new entrants (Guangde Qingna's 20 GWh Sichuan project, Jiangsu Zoolnasm's 20 GWh) illustrate the domestic build-out. Sinopec partnered with LG Chem on sodium cathode/anode materials. [24] ESS News

3.2 Western and other players

- Natron Energy (USA, private). The cautionary tale. First US commercial-scale SIB producer (Holland, Michigan, PBA chemistry, UL 1973 listed), with a $1.4bn, 24 GWh North Carolina gigafactory (Rocky Mount, Edgecombe County) announced August 2024. Its board voted to shut down on August 27, 2025 after failing to secure funding; all 95 employees across its Michigan and California facilities received WARN Act notices and operations ceased September 3, 2025, halting the North Carolina project (assets went to Sherwood Partners). A discontinued program is evidentially significant: it demonstrates that first-mover Western SIB manufacturing failed to secure demand and capital even with ARPA-E and IRA support. [15]

- Peak Energy (USA, private). Denver-based, founded 2023, $55m Series A (Xora/Temasek, August 2024). Deployed the first US grid-scale SIB system (3.5 MWh, NFPP, passively cooled, SolarTAC Colorado, 2025), signed a >$500m / up to 4.75 GWh deal with Jupiter Power (720 MWh in 2027), a 1.5 GWh Energy Vault data-center deal (February 2026), and a strategic partnership with GM (which will develop the cell in Michigan and retain manufacturing rights). [16]

- Faradion (UK, owned by Reliance Industries, NSE:RELIANCE). Sodium pioneer (founded 2010), acquired by Reliance for ~£100m enterprise value (fully consummated October 2024). Technology destined for Reliance's Dhirubhai Ambani Green Energy Giga Complex in Jamnagar; Mukesh Ambani targeted production commencing in the second half of 2025-2026. Holds foundational zero-volt transport IP. [17][26]

- Tiamat (France, private). CNRS spin-off, NVPF polyanionic chemistry, the first company to commercialize SIB in an electrified product (power tools). Building a 5 GWh Amiens gigafactory (first phase 700 MWh); investors include Stellantis, Arkema, MBDA, Bpifrance. Phase-one commissioning slipped from 2025 toward 2026. [18]

- Altris (Sweden, private). Uppsala spin-off, Prussian white cathode plus proprietary NaBOB fire-retardant electrolyte, ~160 Wh/kg. Volvo Cars Tech Fund, Clarios, and Maersk Growth invested in the B1 round; Volvo explicitly notes SIBs are not planned for its EVs, only BESS. Building CAM capacity in Kolín (Czech Republic). [19]

3.3 Automaker adoption status

Only two production passenger models have materialized: JAC's Yiwei/Sehol (HiNa, low volume, 2024) and the forthcoming Changan Nevo A06 (CATL, mid-2026). Western automaker engagement (Volvo, Stellantis, GM) is confined to stationary storage or venture investment, not vehicle deployment. This gap between announcement and production is itself a finding. [13][16][19]

3.4 Upstream material suppliers

Prussian blue: Arxada (Switzerland, supplied Natron), Draslovka (Czech Republic). Cathode active materials and hard carbon are overwhelmingly Chinese; Altris (Prussian white) is the only at-scale European CAM producer. [15][19]

4. Economics and Market Dynamics

4.1 The cost-advantage claim, examined

The headline case for SIBs rests on material abundance, but the peer-reviewed evidence is markedly more sober than promotional figures suggest. The definitive analysis is Yao, Benson and Chueh (Nature Energy, 2025), which modeled 6,048 techno-economic scenarios using Argonne's BatPaC v5.1.

- At ~$10,000/tonne lithium carbonate equivalent (LCE) (roughly 2024-25 levels), the study finds "virtually no Na-ion development scenarios that will result in a Price Advantage condition without a coinciding supply chain disruption in graphite." [4]

- If lithium prices rise by 2027 and remain high at ~$50,000/tonne LCE, "over 55% of all Na-ion technical roadmaps lead to a Price Advantage condition before 2035" (defined as >80% probability of being cheaper than LFP). [4]

- Over 40% of scenarios reach "price parity" (≥20% probability) on or before 2030, but the authors explicitly caution against assuming near-term (pre-2030) price advantage over LFP. [4]

- The single largest lever is not manufacturing learning rate but SIB energy density, because higher density reduces materials intensity per kWh. [4]

This reframes the entire debate. SIB economics are a leveraged bet on lithium prices, not an unconditional cost win.

4.2 Current price reality

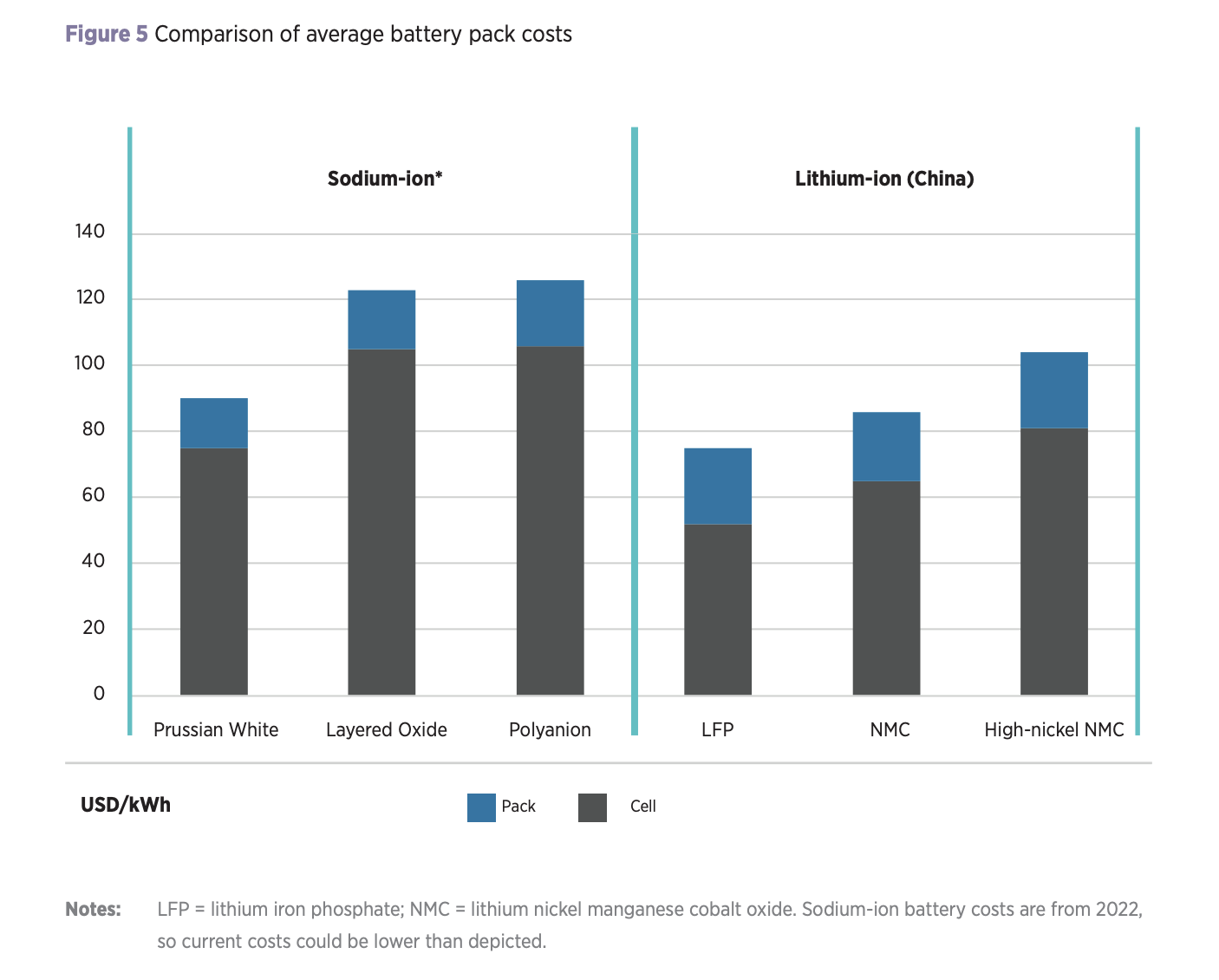

At early-2026 prices, SIBs still carry a premium over LFP, contradicting much promotional material. HiNa's Li Shujun stated that lithium cells run 0.3-0.5 yuan/Wh (~$44-73/kWh) while sodium cells run 0.5-0.7 yuan/Wh (~$70-100/kWh), with convergence expected around 2027. For LFP, BloombergNEF's 2025 survey (published December 9, 2025) recorded Li-ion pack prices falling 8% to a record $108/kWh average, with the lowest observed LFP cell at $36/kWh and stationary packs at $70/kWh (down 45% year-on-year, making stationary storage the cheapest segment for the first time). Peer-reviewed process-based cost modeling (Ruppert et al., CellEst 3.0, 2025) puts NaNFM SIB cells at $54-62/kWh (cylindrical as low as $46/kWh), competitive with but not decisively below LFP. [7][8][21]

The structural point from techno-economic literature (anchored by Vaalma, Buchholz, Weil and Passerini, Nature Reviews Materials, 2018) is that in SIBs the anode (hard carbon) and separator become the most expensive components, inverting the LIB cost structure where the cathode dominates. Hard carbon active material (~$15/kg) is more expensive than natural graphite (~$10/kg) and, at lower density and capacity, requires more material and electrolyte. The SIB material saving is concentrated in the cathode and in aluminum-for-copper current collectors; the anode side partially offsets it. [6]

4.3 The lithium price whipsaw

The macro backdrop turned in SIBs' favor in late 2025. Lithium carbonate rose more than 50% in three months to exceed 110,000 yuan (~$15,700)/tonne by late December 2025, and the IEA noted early-2026 lithium prices were more than double year-earlier levels (though still ~70% below the 2022 peak), driven partly by the suspension of CATL's Jianxiawo mine and surging storage demand. Cobalt also doubled after the DRC's export ban. If sustained, this is precisely the condition Yao et al. identify as reviving the SIB case, and it explains the observed 2026 acceleration of sodium programs. [2][4]

4.4 Manufacturing capacity versus utilization

The capacity picture is one of large announcements and low utilization. Benchmark Mineral Intelligence put installed SIB production capacity at ~123 GWh by end-2025 (over 95% in China) but flags low utilization rates and depressed prices as the critical commercialization challenge. IRENA cites ~70 GWh in 2025 rising to 400 GWh by 2030. The IEA's framing is the most sobering: current SIB cell manufacturing capacity equals just over 1% of lithium-ion capacity, and announced 2030 SIB projects amount to only about 7% of committed lithium-ion capacity for that year. Not all projects proceed: Kingshine cancelled a 6 GWh Jiangxi plant (February 2024) and Veken Tech postponed a 2 GWh project. [2][3][9][23]

4.5 Demand forecasts and their divergence

Forecasts diverge by more than an order of magnitude, and the divergence is instructive:

- China domestic: ~10 GWh (2025) to 292 GWh (2034), ~45% CAGR (industry/CESA). [23]

- Global market share: Benchmark Mineral Intelligence, citing the evaporated cost advantage, projects SIBs make up less than 1% of the global battery market today and "at best" reach 15.5% of the market in the next ten years. [24]

- Global capacity: IRENA ~400 GWh by 2030; IEA notes announced 2030 capacity is only ~7% of lithium-ion's. [2][3]

- Demand range: annual demand projections span 50-600 GWh by 2030, a 12-fold variance. [23]

The driver of divergence is almost entirely the assumed lithium price path and the pace of hard carbon scale-up. Optimistic forecasts assume sustained high lithium and rapid anode maturation; conservative ones assume continued LFP cost declines (which BNEF's data confirm are ongoing). The honest conclusion is a wide cone of uncertainty centered on a niche-to-meaningful trajectory, not displacement of lithium-ion. [8][24]

5. Supply Chain and Materials

5.1 The de-risking: no lithium, cobalt, or (mostly) nickel

SIBs eliminate lithium entirely and, in iron- and manganese-based chemistries (PBA, NFPP, LFP-analog oxides), cobalt and nickel as well. Sodium is sourced from soda ash (sodium carbonate) and sodium hydroxide via the mature, globally distributed Solvay process and salt electrolysis. This is a real diversification: soda ash production is geographically dispersed, and the raw material is price-stable and tariff-resistant in a way lithium is not. [3][24]

5.2 The reintroduced and residual dependencies

- Hard carbon anode. The critical vulnerability. Industrial-scale hard carbon faces a precursor bottleneck: biomass precursors (coconut shell, agricultural waste) yield only ~2.5% battery-grade carbon by mass, while coal/anthracite processing yields ~45%. Chinese producers are consequently shifting to domestic coal precursors, with hard carbon costs reported below 30,000 yuan (~$4,400)/tonne. Production capacity is limited to several thousand tonnes and heavily concentrated in China; the IEA explicitly names hard carbon as a poorly developed, China-concentrated supply chain. This is where the "supply chain resilience" narrative is weakest. [1][25]

- Vanadium (NVPF). Tiamat's first-generation NVPF depends on vanadium, a genuinely constrained material; this is why NFPP (iron-based) is gaining favor. [5][18]

- Cathode and precursor manufacturing. Even where materials are abundant, the processing and CAM synthesis is overwhelmingly Chinese. [25]

5.3 Net assessment

The resilience advantage is partial. SIBs relocate rather than eliminate dependency: they trade lithium/cobalt/nickel exposure for hard carbon (and, in some chemistries, vanadium) exposure, and both the anode and cathode processing remain China-concentrated. For a Western or Indian actor, adopting SIB improves raw-material diversity but does not by itself confer supply-chain independence unless a domestic hard carbon and CAM base is built in parallel. Altris's all-European Prussian white supply chain and Peak's US soda-ash-to-cell ambition are the exceptions that prove the rule. [16][19]

6. Regulatory Landscape

This dimension is genuinely limited and should be treated briefly. There is little SIB-specific regulation; SIBs are largely governed by the same frameworks as LIBs:

- Transport: UN 38.3 governs battery transport. SIB's zero-volt capability is a practical safety and logistics advantage within this framework rather than a regulatory carve-out, though Faradion (acquired by Reliance Industries) and others hold IP on zero-volt safe transport. [26]

- EU: The EU Battery Regulation (carbon footprint, recycled content, due diligence) applies to SIBs as to LIBs. Notably, SIBs' lower cradle-to-gate carbon footprint (hard carbon at 3.2 kg CO₂-eq/kg vs. synthetic graphite at 25.1) can help meet these requirements, and the EU Critical Raw Materials Act creates a structural preference for lithium-free chemistries, which Altris and others explicitly invoke. [5][19]

- China: The decisive regulatory event is GB 38031-2025, the traction-battery safety standard (effective July 1, 2026), requiring no fire/no explosion for two hours; CATL's Naxtra was the first SIB to certify. Chinese five-year-plan industrial policy explicitly supports sodium alongside lithium. [12]

- US: IRA/ARPA-E support underwrote Natron and Peak; the shift toward foreign-entity-of-concern (FEOC) rules and tariff volatility is increasing interest in non-Chinese-input chemistries, indirectly favoring domestic SIB. [15][16]

No SIB-specific incentive structure of material weight exists outside general battery and EV policy. The regulatory story is one of favorable-by-default treatment, not bespoke support.

7. Geopolitical and Strategic Dimensions

7.1 Chinese concentration

China's ownership in SIB is more extreme than in lithium-ion. Nearly all existing global SIB capacity is Chinese (Benchmark: over 95% installed; IEA: more than 95% of 2030 capacity), and China leads SIB patenting decisively. The Carnegie Endowment's 2026 battery-geopolitics analysis documents a sodium-ion patent filing surge since 2022 that outpaced even lithium-ion's 2014 peak, with China holding ~43% of total battery patents in 2024 (Europe 21%, US 18%, South Korea 10%, Japan 2%). SIB is a deliberate pillar of Chinese industrial strategy: it reduces China's own residual lithium-import dependency (China holds only ~6.3% of global lithium reserves) while extending its manufacturing and IP dominance into the next chemistry. [1][9][10]

7.2 The strategic paradox for the West

SIB is simultaneously an opportunity and a trap for Western and Indian actors. The opportunity: sodium's abundance and the drop-in compatibility with existing LIB manufacturing lines make it, in principle, the most onshorable battery chemistry, and the one least exposed to Chinese-controlled lithium refining. The trap: if Western firms adopt Chinese SIB cells, materials, or IP, they build strategic infrastructure (grid storage, backup power) dependent on continued Chinese cooperation, and China's patent thicket raises the barrier to independent development. Natron's collapse shows how hard independent Western manufacturing is even with policy support. [10][15]

7.3 Does SIB alter critical-mineral dependency, or relocate it?

The honest answer is: partially alters, mostly relocates in the near term. SIB genuinely removes lithium, cobalt, and nickel from the equation, a strategically meaningful reduction in exposure to the most concentrated and volatile mineral markets. At current maturity it substitutes dependence on China-concentrated hard carbon and CAM processing. The strategic prize (true supply-chain de-risking) is achievable only if Western/Indian actors build domestic anode and cathode capacity, which no one has yet done at scale. India's Reliance/Faradion bet is the most vertically integrated attempt to convert the sodium opportunity into independence. [1][17][25]

8. Risk Matrix

| Risk | Category | Likelihood | Impact | Credible mitigations |

|---|---|---|---|---|

| LFP cost declines continue, erasing SIB cost case | Competitive/Market | High | High | Target cold-climate and safety niches where SIB wins independent of price; hybrid packs; ride sustained high lithium |

| Lithium prices stay low (~$10k/t LCE) | Market | Medium | High | Focus on non-cost advantages (0V transport, low-temp, cycle life); avoid pure cost-parity positioning |

| Hard carbon supply fails to scale / stays China-concentrated | Supply chain / Technological | High | High | Invest in coal- and biomass-precursor hard carbon; qualify multiple suppliers; treat as top scouting priority |

| Volumetric energy density gap never closes vs. NMC | Technological | High | Medium | Concede long-range EV segment; concentrate on stationary and entry EV |

| Chinese manufacturing/IP dominance locks out Western entrants | Geopolitical | High | High | Build domestic CAM/anode base; license non-Chinese IP (Faradion, Altris); government procurement preference |

| Western SIB ventures fail on demand/capital (Natron precedent) | Market/Competitive | Medium-High | Medium | Anchor offtake before capacity build (Peak's shared-pilot model); strategic-investor validation (GM-Peak) |

| Layered-oxide thermal runaway / cycle-life shortfall | Technological/Safety | Medium | Medium | Prefer polyanionic/PBA for safety-critical stationary; rigorous cell qualification |

| Manufacturer specs (energy density, cycle life) fail to replicate in field | Technological | Medium | Medium | Independent third-party validation; treat asserted specs cautiously |

| Overcapacity / low utilization depresses returns | Market | High | Medium | Avoid speculative capacity; scale with contracted demand |

| Vanadium constraint (NVPF chemistries) | Supply chain | Medium | Low-Medium | Shift to iron-based NFPP; already underway industry-wide |

Risks not included because the topic does not support them: no material SIB-specific regulatory prohibition risk exists, and there is no credible near-term risk of SIB displacing lithium-ion (so "disruption of incumbent" is not a risk to model).

9. Strategic Recommendations

9.1 For institutional investors evaluating exposure

- Treat SIB as a leveraged lithium-price hedge, not a secular growth story. The peer-reviewed evidence (Yao et al.) is unambiguous: SIB economics are contingent on sustained lithium prices well above 2024-25 lows. Size positions accordingly. The threshold that would change this recommendation: lithium carbonate holding above ~$30,000/tonne LCE for more than four consecutive quarters, or a demonstrated hard carbon cost breakthrough below ~$3,000/tonne at scale. [4]

- Prefer exposure through diversified incumbents (CATL, BYD) over pure-play SIB startups. The incumbents carry chemistry optionality and can absorb the demand-timing risk that killed Natron. Pure-plays require contracted offtake before capacity commitment as a hard due-diligence gate. [13][15][20]

- In the West, favor stationary-storage-focused players with anchor offtake and strategic validation (Peak, post-GM) over EV-cell aspirants. Avoid pure-play graphite anode suppliers, which face hard carbon substitution risk in any SIB upside scenario. [16]

- Watch hard carbon as the leading indicator. Supplier scale-up, precursor economics, and any non-Chinese capacity are the datapoints that de-risk the entire thesis. [1][25]

9.2 For industrial and automotive strategists evaluating adoption or manufacturing entry

- Adopt SIB now where the win is non-cost: stationary storage in cold climates, industrial/telecom backup, micro-mobility, and lead-acid replacement. These segments reward SIB's demonstrated advantages (0V transport, low-temperature performance, cycle life, safety) regardless of the lithium price path. [1][14][16]

- For automakers, pursue SIB via dual-chemistry/hybrid packs and entry-level urban models, not flagship EVs. The Changan Nevo A06 and CATL Freevoy architecture are the templates. Do not position SIB against long-range NMC; the volumetric physics does not support it. [2][12][13]

- If entering manufacturing, exploit drop-in compatibility with existing LIB lines to minimize capex, but secure domestic hard carbon and CAM supply as a precondition, not an afterthought. Natron's failure was demand and capital, not technology; Tiamat's and Reliance's slippage is execution and scale-up. Anchor demand contractually before building capacity. [5][15][18]

- For Western/Indian actors, treat SIB as the most viable route to genuine battery supply-chain sovereignty, but only if paired with domestic anode/cathode investment. Adopting Chinese SIB cells relocates rather than reduces strategic dependence. License non-Chinese foundational IP (Faradion under Reliance, Altris) and align with EU Critical Raw Materials Act / US FEOC preferences. The benchmark that would justify accelerated entry: a national procurement mandate or FEOC-linked incentive that guarantees offtake for domestically produced non-Chinese SIB. [17][19]

10. Caveats and Confidence

- Manufacturer-announced performance figures (CATL Naxtra 175 Wh/kg, >10,000 cycles, 90% at -40°C; HiNa 165 Wh/kg, 8,000 cycles) are asserted and not independently verified; safety certification (GB 38031-2025) is verified but performance specs are not.

- Cost and price figures are volatile and source-dependent; the lithium price path is the dominant swing variable and is itself uncertain.

- Market forecasts diverge 12-fold; this report presents ranges rather than point estimates by design.

- Several widely circulated figures (e.g., "hard carbon = 35-45% of cell material cost," "$55-70/kWh SIB cells at a 35-40% discount to LFP," specific CATL Naxtra $/kWh figures) originate from vendor blogs and analyst notes and could not be corroborated by peer-reviewed or primary institutional sources; they are flagged rather than relied upon. No peer-reviewed source was identified for a precise hard carbon cost-share percentage.

- The report's forward-looking statements reason from current evidence and are labeled as such; they are not predictions.

References

- International Energy Agency. 2026. "Sodium-ion battery momentum grows, but challenges remain." IEA, Paris.

- International Energy Agency. 2026. "Electric vehicle batteries – Global EV Outlook 2026." IEA, Paris.

- International Renewable Energy Agency. 2025. "Sodium-Ion Batteries: A Technology Brief." IRENA, Abu Dhabi.

- Yao, Adrian, Sally M. Benson, and William C. Chueh. 2025. "Critically assessing sodium-ion technology roadmaps and scenarios for techno-economic competitiveness against lithium-ion batteries." Nature Energy 10 (3): 404-416.

- Voß, Philipp, Benedikt Gruber, Miriam Mitterfellner, Jan-Darius Plöpst, Florian Degen, Richard Schmuch, and Simon Lux. 2025. "Benchmarking state-of-the-art sodium-ion battery cells – modeling energy density and carbon footprint at the gigafactory-scale." Energy & Environmental Science 18 (17): 8104-8129.

- Vaalma, Christoph, Daniel Buchholz, Marcel Weil, and Stefano Passerini. 2018. "A cost and resource analysis of sodium-ion batteries." Nature Reviews Materials 3: 18013.

- Ruppert, Julius, Philipp Voß, et al. 2025. "Analyzing material and production costs for lithium-ion and sodium-ion batteries using process-based cost modeling – CellEst 3.0." Journal of Power Sources / ScienceDirect.

- BloombergNEF. 2025. "Lithium-Ion Battery Pack Prices Hit Record Low." BNEF Annual Battery Price Survey (December 9, 2025).

- Benchmark Mineral Intelligence. 2025. "The state of play of next-generation battery capacity in 2025."

- Carnegie Endowment for International Peace. 2026. "Battery Geopolitics: Balancing Industrial Power in the Race to Store Energy."

- Degen, Florian, et al. 2025. "Comparative life cycle assessment of lithium-ion, sodium-ion, and solid-state battery cells for electric vehicles." Journal of Industrial Ecology.

- CATL. 2025. "Naxtra Battery Breakthrough & Dual-Power Architecture." CATL press release.

- CATL. 2026. "CATL and CHANGAN Launch World's First Mass-Production Sodium-Ion Passenger Vehicle." CATL press release.

- CnEVPost. 2024. "'World's largest' sodium-ion battery energy storage project goes into operation in China."

- Manufacturing Dive. 2025. "Sodium-ion battery maker Natron Energy shuts down, halts $1.4B factory plans"; Energy-Storage.news. 2024. "Natron Energy starts manufacturing '50,000+ cycle-life' sodium-ion batteries at Michigan factory."

- ESS-News / pv magazine. 2025. "Peak Energy launches first U.S. grid-scale sodium-ion storage system"; Electrek. 2025. "Peak Energy's $500M deal will deploy the world's largest sodium-ion battery system"; Latitude Media. 2026. "What does the GM-Peak Energy partnership mean for sodium-ion?"

- Energy-Storage.news. 2024. "Non-lithium alternatives: Reliance completes sodium-ion acquisition [Faradion]."

- pv magazine / ESS-News. 2024-2025. "Tiamat secures funding for sodium-ion gigafactory in France"; "Consultation over 5 GWh French sodium-ion battery factory."

- Altris AB / Cision. 2025. "Altris announces investment and collaboration with Volvo Cars."

- Power Technology. 2024. "BYD breaks ground on new sodium-ion battery facility in China"; electrive.com. 2026. "BYD makes advances in sodium-ion and solid-state batteries."

- CnEVPost / CarNewsChina. 2025-2026. HiNa Battery commercial-vehicle and cost-parity disclosures (Li Shujun).

- CRU Group. 2025. "China's overcapacity: Will its battery industry consolidate?"

- IDTechEx. 2025. "Sodium-ion Batteries 2025-2035: Technology, Players, Markets, and Forecasts"; ESS-News. 2025. "Massive 20 GWh sodium-ion battery manufacturing plant announced in China."

- C&EN (American Chemical Society). 2025. "Sodium-ion batteries: Should we believe the hype?"

- ScienceDirect. 2025-2026. Hard carbon anode reviews (precursors, bottlenecks); Journal of Energy Storage. 2025. "Sodium-ion battery cost projections and their impact on the global energy system transition until 2050."

- Faradion. "Superior Safety" (zero-volt transport); Rudola, A., et al. 2022. "Zero volt storage of Na-ion batteries." Journal of Power Sources.