SpaceX IPO: What $1.77 Trillion Actually Buys (SPCX)

Our sum-of-the-parts finds $700B–$1.1T of reasonable value in SPCX. The remaining trillion rests on Starship, orbital compute, and Grok.

SpaceX (Nasdaq: SPCX): Post-IPO Valuation and Long-Term Growth Potential into the Next Decade and Beyond

TL;DR

- SpaceX completed the largest IPO in history on June 12, 2026, pricing 555,555,555 Class A shares at a fixed $135.00 to raise roughly $75 billion at an implied valuation near $1.77 trillion, a multiple of roughly 95 times trailing 2025 revenue against a reported net loss of about $4.9 billion [1][2][5].

- The valuation is not supported by demonstrated cash generation alone; our transparent sum-of-the-parts places the defensible, evidence-backed value of the connectivity, launch, and AI businesses at roughly $700 billion to $1.1 trillion, meaning the remaining $700 billion to roughly $1 trillion rests on optionality (Starship at target cost, orbital data centers, and frontier-scale AI) rather than realized results [12][18].

- The two variables that most govern the outcome are whether Starship reaches reliable, rapidly reusable, high-cadence operation at its target marginal cost, and whether the recently acquired xAI segment narrows its losses; the AI segment lost $6.4 billion from operations in 2025 and, per Data Center Dynamics, "lost $2.4 billion in the three months to March 2026, up from $936 million a year ago" [1][14][17]. Founder supermajority voting control (over 82 percent) means public shareholders own the exposure but cannot direct capital allocation [1].

1. Executive Summary

On June 12, 2026, Space Exploration Technologies Corp. began trading on the Nasdaq Global Select Market and the new Nasdaq Texas exchange under the ticker SPCX, completing the largest initial public offering in financial history [2][5]. Underwriters were granted a 30-day option to purchase up to an additional 83,333,333 Class A shares at the IPO price [51]. These terms are confirmed against the SEC registration statement and primary financial reporting of record and are treated here as established fact [1][2][5].

The central analytical tension is unambiguous. At roughly 95 times trailing sales and against a reported 2025 net loss of approximately $4.9 billion, SPCX is priced for outcomes it has not yet demonstrated [12][13]. Our assessment is that the IPO valuation is not justified by demonstrated results and is justified only under a specific, demanding set of forward assumptions. The demonstrated business, Starlink connectivity plus a dominant launch franchise, plausibly supports several hundred billion dollars of value; the gap to $1.77 trillion is option value on Starship economics, orbital AI compute, and xAI's competitive position [12][18][14].

A critical fact reframes what is being valued. Effective February 2, 2026, SpaceX acquired X.AI Holdings Corp. (xAI), which had itself acquired the social platform X in March 2025; because these were transactions between entities under common control, SpaceX's financial statements have been retrospectively recast to consolidate xAI and X for all periods presented [1]. The $1.77 trillion therefore values a three-segment conglomerate (Connectivity, Space, and AI), not a pure-play space company [1][14].

The growth thesis rests on three legs of very different maturity: (1) Starlink, the demonstrated cash generator, with about $11.4 billion of 2025 revenue at a roughly 63 percent segment EBITDA margin [12][19]; (2) the launch franchise, the demonstrated technical and strategic moat but a comparatively low-margin, capital-intensive business [13][15]; and (3) the AI segment and Starship, both pre-monetization or pre-operational at scale and accounting for the bulk of capital intensity and losses [14][17].

Bull, base, and bear framing in compressed form: the bull case (associated with investor Ron Baron, who told CNBC in May 2026 that SpaceX "is going to become the largest company on the planet" and "over the next 10 or 15 years is going to be worth $10 trillion, $20 trillion, $30 trillion, and I could be very low") requires Starlink to scale to tens of millions of subscribers, Starship to reach operational reusability at low marginal cost, and the AI segment to compete at the frontier [44][45]. The base case sees Starlink continuing to compound while Starship matures over several years and AI losses persist, leaving the stock range-bound to modestly higher and exposed to multiple compression. The bear case, articulated by Morningstar analyst Nicolas Owens at a $63 fair-value estimate (a 53 percent discount to the IPO price, implying roughly $780 billion), treats the optionality as largely unproven and the price as a mathematical overreach; Owens stated "our valuation is the result of mathematics more than skepticism," assigning the optimistic $1.97 trillion ($154/share) "moonshot" scenario only a 7 percent probability [18][43].

2. The Offering and Post-IPO Structure

2.1 Confirmed terms

The offering is confirmed as follows against the prospectus and reporting of record. Ticker: SPCX, listed on Nasdaq and dual-listed on Nasdaq Texas, the first such dual opening-bell ceremony in Nasdaq history [5][6]. First trading day: June 12, 2026, with final pricing set after the close on June 11 and the offering expected to close on or about June 15, 2026 [51][2]. Greenshoe: an underwriter option for up to 83,333,333 additional Class A shares at the IPO price, exercisable for 30 days [51].

The underwriting syndicate is large. The prospectus lists Goldman Sachs & Co. LLC as the lead, with Morgan Stanley, BofA Securities, Citigroup, and J.P. Morgan as additional joint book-running managers, followed by Barclays, Deutsche Bank, RBC, UBS, Wells Fargo, and a further tier including Allen & Company, Cantor, Needham, Raymond James, Société Générale, Stifel, William Blair, BTG Pactual, ING, Macquarie, Mirae Asset, Mizuho, and Santander [1]. The reported syndicate of roughly 21 to 23 banks is consistent with this list [12]. A standard post-IPO analyst quiet period applies to syndicate members before they may publish initiation-of-coverage research.

The offering was structured with an unusually large retail allocation reported at up to 30 percent (approximately $23 billion of market value), versus the typical 10 percent or less, distributed through brokerages including Charles Schwab, Fidelity, Robinhood, SoFi, and Morgan Stanley's E-Trade [43]. The deal was reported to be roughly 3.3 times oversubscribed [43].

2.2 Capital structure and dual-class voting control

Following the offering, SpaceX has two classes of common stock outstanding for public purposes (a third class, Class C, also exists per the recast share-split disclosures). Class A carries one vote per share; Class B carries 10 votes per share [1]. Founder, CEO, Chief Technical Officer, and Chairman Elon Musk holds a supermajority of voting power, reported at over 82 percent, through his Class B ownership and additional holdings [1][53]. Class B holders are entitled to elect a majority of the board. As a result, SpaceX qualifies as a "controlled company" under Nasdaq corporate governance rules and intends to rely on exemptions from certain governance requirements [1]. All share and per-share figures reflect a five-for-one stock split effective May 4, 2026 [1].

The practical consequence is decisive: public Class A shareholders provide capital and bear economic exposure but hold negligible influence over corporate direction, board composition, or capital allocation, including the long-duration, low-near-term-return programs (Starship and Mars architecture) that the founder prioritizes [1].

2.3 The valuation perimeter and the xAI combination (resolved)

This item is resolved, not left open. The prospectus states plainly that SpaceX's consolidated financial statements have been retrospectively recast to include the historical results of X.AI Holdings Corp., acquired effective February 2, 2026 (the "xAI Merger"), and X Holdings Corp., acquired by xAI effective March 28, 2025 (the "X Merger"), because these were transactions between entities under common control [1]. The combination was an all-stock transaction; the merger converted each xAI share into 0.1433 of a SpaceX share, and the deal was reported in February 2026 to value the combined entity at roughly $1.25 trillion (about $1 trillion attributed to SpaceX and roughly $250 billion to xAI) [9][10][11].

The prospectus defines an "AI segment" comprising the AI compute business, the Grok frontier model, and X [1]. This materially changes the valuation perimeter: the $1.77 trillion values a space, connectivity, and AI conglomerate. In 2025 the AI segment contributed approximately $3.2 billion of revenue (about 17 percent of the total) but an operating loss of roughly $6.4 billion, making it the dominant driver of the consolidated net loss [16][17]. The valuation question therefore cannot be answered without separating connectivity and launch (profitable, demonstrated) from AI (loss-making, capital-hungry, speculative).

2.4 Float, lockups, quiet period, and index treatment

The public float at listing is deliberately tight, reported at roughly 4 percent of total equity, or approximately $70 billion of tradeable stock against the roughly $1.77 trillion capitalization [12][53]. With a float this thin, modest order-flow imbalances move the price substantially, and first-day price discovery reflects order-book mechanics as much as fundamental conviction [53].

The lockup structure is unusual and staggered rather than a single 180-day cliff [40][41]. Per the S-1, after the first post-IPO quarterly earnings report (the April-June period), insiders may sell up to 20 percent of eligible locked-up shares, with an additional 10 percent unlocking if the stock trades at least 30 percent above the IPO price for a specified number of sessions; five time-based tranches of 7 percent each release at 70, 90, 105, 120, and 135 days; a further 28 percent unlocks after the July-September earnings report; and the remainder releases at 180 days [40][42]. Musk and select major backers are subject to a longer 366-day lockup, and Musk is carved out of the accelerated schedule entirely [41]. A reported 5 percent friends-and-family carve-out (roughly $3.75 billion) carries no lockup and can trade from day one [42].

This structure was engineered substantially to expand the public float quickly enough to maximize index weighting under fast-track inclusion rules [41][42]. On index treatment: MSCI announced early inclusion beginning June 13, 2026 (T+1) [12]; the Nasdaq-100 "fast entry" provision (effective May 1, 2026) makes SPCX eligible after 15 trading sessions, around July 7, 2026 [40][52]; Russell 1000 inclusion moves to roughly five trading days post-IPO [41]. S&P 500 inclusion is excluded for now: S&P Dow Jones Indices declined to change its rules, which require 12 months of trading and four consecutive quarters of GAAP profitability, neither of which SpaceX meets [41][43].

2.5 Realized first-day trading (date-stamped, provenance-labeled)

Pre-open indications on June 12, 2026 pointed to an opening print well above the IPO price, reported in the range of $169 to $175 per share, roughly 25 to 30 percent above $135 [4][2]. Reuters reported the same morning that the stock was "on course to blow past $2 trillion" in market value, which is forward-looking language and not a confirmed close [3]. A SpaceX-linked perpetual futures contract (SPCX-USDC) on the Hyperliquid venue traded around $172 intraday, about 27 percent above the IPO price, but this is a crypto derivative proxy and not the Nasdaq equity print [2]. As of the latest reporting available at the time of writing, the official Nasdaq opening cross, intraday high and low, and 4:00 p.m. ET closing price had not yet been published, and any confirmed first-day close and resulting market capitalization should be taken from post-close reporting of record and date-stamped accordingly [2][3]. No qualifying LULD volatility halt had been confirmed at the time of writing, though brokers had flagged halts as likely given the thin float [2].

3. Key Players and Stakeholders

3.1 SpaceX and the founder

SpaceX is simultaneously a launch provider, a satellite-broadband operator, a defense contractor, and now an AI company. The founder is a distinct, first-order analytical factor: his supermajority voting control, his concentration of decision rights over capital allocation, and the reputational and political exposure he carries are all material to the equity [45][50]. The prospectus discloses hundreds of millions of dollars of expected legal costs tied to xAI, Grok, copyright, data-privacy, and deepfake-related matters, and explicitly acknowledges that investor sentiment toward Musk himself is a risk factor [50]. President and COO Gwynne Shotwell and CFO Bret Johnsen rang the opening bell in New York while Musk rang it from Starbase, Texas [5][6].

3.2 Customers

The U.S. government is the anchor customer across multiple segments. NASA relies on SpaceX as its primary launch and crew-transport partner; in 2025 SpaceX flew all five U.S. crew and cargo missions to the International Space Station [19]. The Department of Defense, Space Force, and National Reconnaissance Office are central: SpaceX flew 11 of 12 National Security Space Launch missions in 2025 [19]. Commercial satellite operators and rideshare customers form a third group. On the connectivity side, Starlink served 10.3 million subscribers across 164 countries as of March 31, 2026, spanning consumer, enterprise, maritime, aviation, and government users [1][14].

3.3 Shareholders, banks, and strategic holders

New public Class A shareholders include a large retail cohort and index funds forced to buy via fast-track inclusion [41]. Early holders benefiting from the listing include Valor Equity Partners (whose CEO Antonio Gracias sits on the board and held a reported 503.4 million Class A shares, about 7.3 percent, pre-IPO), Founders Fund's Luke Nosek, Ron Baron, Cathie Wood's ARK Invest, and Fidelity [2][44]. EchoStar is a reported strategic holder with an estimated 3 percent stake, acquired through the spectrum transactions discussed in Section 4 [2][35]. Gulf sovereign wealth funds placed multibillion-dollar orders in the book [2].

3.4 Competitors and regulators

Competitors are addressed in Sections 4 and 7. Regulators (FAA, FCC, and export-control authorities) are addressed in Section 6. Both genuinely shape outcomes and are treated there to avoid duplication.

4. Technical and Operational Considerations

4.1 The launch fleet and demonstrated reusability economics

SpaceX operates the most active launch fleet in history. In 2025 it conducted 165 Falcon 9 launches, more than the rest of the world combined and about 85 percent of the U.S. total, plus five suborbital Starship tests, a sixth consecutive annual record; per SpaceNews, "in 2025, SpaceX flew 165 Falcon 9 missions, more than the rest of the world combined... the United States and China accounted for 88% of all orbital launches" [27][28]. As of June 11, 2026, the Falcon family had flown 661 times with 658 full successes, a 99.55 percent success rate (the active Block 5 variant at 99.83 percent) [26]. One booster (B1067) has flown 35 times, 55 boosters have flown multiple missions, and fairing halves have been reflown more than 300 times [26]. For 2026, management guided to roughly 140 to 145 Falcon 9 launches, a deliberate plateau as the manifest shifts toward Starship [26][27].

Reusability economics, labeled by provenance: the list price of a Falcon 9 launch is approximately $62 million (company-advertised) [25]. Musk has stated a best-case marginal cost near $15 million and booster refurbishment cost near $1 million [25]. ARK Invest modeled, from turnaround-time data, that first-stage refurbishment cost fell from roughly $13 million to roughly $1 million over five years and estimated cost-per-kilogram to low-Earth orbit at roughly $800 for a reused Falcon 9 versus roughly $2,700 for a new one (modeled estimates, not disclosed figures) [24]. These figures are directionally corroborated by multiple analysts but are not audited prospectus disclosures and should be treated as modeled or asserted rather than measured [23][24]. The Dragon crew capsule has carried 78 astronauts since 2020 (company figure) [19].

4.2 Starship: demonstrated milestones versus stated goals

Starship is the single most important long-term variable, and its status must be stated with care to separate demonstrated milestones from aspiration.

Demonstrated, as of late May 2026: Starship had flown 12 integrated flight tests, with seven successes and five failures [20]. The booster catch by the launch tower's mechanical arms was first demonstrated on Flight 5 in October 2024 [20]. Flight 12, launched May 22, 2026, was the maiden flight of the upgraded Version 3 (Block 3) architecture; it deployed about 20 mock Starlink satellites and achieved a controlled splashdown of the upper stage in the Indian Ocean, but the Super Heavy booster suffered a mishap during its return and was lost, triggering an FAA-overseen investigation [21][22]. Vehicle specifications (company figures): Super Heavy stands 71 meters with up to 33 Raptor engines producing about 74 meganewtons of thrust; the upper stage is 50 meters with six Raptors; the full stack is about 122 meters; expendable payload to LEO exceeds 100 metric tons [20].

Projected and aspirational, labeled as such: SpaceX states Starship could eventually reduce launch cost by "99 percent or more" and has cited an eventual marginal cost of $2 million to $10 million per flight [25][50]. Management targets operational Starlink payload delivery on Starship in the second half of 2026 and multiple launches per month by late 2026 or 2027 (stated goal) [22][50]. On crewed exploration: NASA reconfigured Artemis III in February 2026 so that it is no longer a crewed lunar landing but a LEO docking demonstration in 2027, with a crewed Artemis IV landing targeted for 2028 using either Starship or Blue Origin's lander, whichever is ready and safer first; SpaceX reports 49 HLS milestones achieved (stated goal and contractual status, not demonstrated landing) [21][22]. Mars timelines, including a reported first interplanetary passenger, are founder aspiration and are not forecasts [22].

The analytical point: a single successful flight, a single booster catch, and a single mock-satellite deployment do not constitute a reliable, rapidly reusable, high-cadence system. The remaining hard problems are repeatability of booster recovery, upper-stage reentry and reuse, reliable engine relight, heat-shield durability, and orbital propellant transfer [20][21].

4.3 Starlink network architecture and capacity

Starlink is the operational and financial core. As of March 31, 2026 it comprised approximately 9,600 broadband and mobile satellites in low-Earth orbit, serving 10.3 million subscribers across 164 countries and representing roughly 75 percent of all active maneuverable satellites in orbit [1][14]. Subscriber growth has been steep: 2.3 million (2023), 4.4 million (2024), 8.9 million (2025), and 10.3 million by March 2026 [14]. Average revenue per user has declined as the base globalized, from a reported $81 per month in 2024 toward roughly $66 per month by the first quarter of 2026, a deliberate trade of ARPU for volume; SpaceX raised some plan prices by up to $10 per month in May 2026, signaling a shift toward monetizing the installed base [15][19].

The direct-to-cell ("Direct to Cell"/D2C) architecture is a distinct, lower-orbit layer of "cell towers in space," with roughly 600 D2C satellites launched since January 2024 [33]. The EchoStar spectrum acquisitions (Section 4.5) are designed to give the next-generation D2C satellites up to roughly 20 times the throughput of the first generation [33].

4.4 The AI segment and its operational relationship to space and connectivity

The AI segment comprises xAI's Grok frontier model, the X platform, and AI compute infrastructure (the Colossus data centers) [1][14]. Operationally, the connecting thesis is "orbital data centers": using Starship's payload capacity to deploy solar-powered, space-based AI compute, with Starlink providing the data link [10][29]. Independent analysts regard the orbital-compute concept as conceivable but many years from material scale; MoffettNathanson's Nick Del Deo called orbital data centers "conceivable" but predicted "many years before anything substantive happens," estimating that 100 GW of orbital compute could require "$4 trillion to $5 trillion" in Nvidia equipment capital expenditure and warning of "a staggering amount of external financing" [11]. Today the relationship is largely financial rather than operational: Starlink's cash flow subsidizes AI capital expenditure, which reached $12.7 billion in 2025 (about 61 percent of group capex) and roughly $7.7 billion in the first quarter of 2026 alone (about 76 percent of group capex) [12][14]. Per SpaceX's S-1 as reported, Anthropic will pay xAI $1.25 billion per month through May 2029, more than $40 billion in total, for the full roughly 300 MW and 220,000-plus Nvidia GPU output of the Colossus 1 data center in Memphis, an arrangement terminable by either party on 90 days' notice [2].

4.5 Vertical integration, manufacturing, and the EchoStar spectrum deals

Vertical integration is SpaceX's principal cost lever: it designs and builds its own rockets, engines, satellites, user terminals, and silicon. Falcon 9 reusability and in-house satellite manufacturing allow Starlink deployment at a cost structure competitors cannot match; roughly three-quarters of 2025 Falcon 9 launches carried SpaceX's own Starlink satellites [15]. In September 2025 SpaceX agreed to acquire EchoStar's AWS-4 and H-block spectrum licenses; per EchoStar's September 8, 2025 Form 8-K, the deal totals "$17 billion, consisting of up to $8.5 billion in cash and up to $8.5 billion in SpaceX stock," plus roughly $2 billion of EchoStar interest payments through November 2027, and a November 6, 2025 amendment added unpaired AWS-3 licenses for approximately $2.6 billion in SpaceX stock [33][34][35]. These deals are confirmed against EchoStar's SEC filing and press release [34]. Securing exclusive spectrum is a durable competitive advantage for the D2C business and the reason EchoStar holds a minority SpaceX stake [35].

5. Economic and Market Dynamics

5.1 The valuation question: a transparent sum-of-the-parts

We reconstruct a sum-of-the-parts to test the $1.77 trillion price. Every input is labeled by provenance and confidence.

Starlink (Connectivity). Demonstrated 2025 revenue of $11.4 billion, operating profit of $4.4 billion, and adjusted EBITDA of $7.2 billion at a roughly 63 percent margin, growing revenue 49.8 percent year over year (prospectus disclosure, high confidence) [12][17]. Applying a generous but defensible 15 to 20 times forward-revenue or roughly 30 to 40 times EBITDA multiple appropriate to a high-growth, high-margin, dominant network yields a standalone value of roughly $450 billion to $600 billion (analyst-estimate range, moderate-to-high confidence) [12]. This is the part of the price most clearly anchored in cash flow.

Space (launch and Dragon). Demonstrated 2025 revenue of $4 billion, up about 8 percent, with a roughly $657 million operating loss driven by approximately $3 billion of Starship R&D (prospectus disclosure, high confidence) [14][17]. As a standalone, low-margin but strategically dominant franchise, a defensible value is roughly $100 billion to $200 billion, with the wide range reflecting how much Starship optionality is attributed here versus treated separately (analyst estimate, moderate confidence).

AI (xAI, Grok, X, compute). Demonstrated 2025 revenue of $3.2 billion and an operating loss of $6.4 billion (prospectus disclosure, high confidence) [17]. The February 2026 merger implied roughly $250 billion for xAI (transaction value, moderate confidence) [9][10]. Given the loss profile and capital intensity, a defensible standalone range is roughly $150 billion to $350 billion, but this is the least anchored leg (speculative, low confidence) [9][14].

Summing the demonstrated and near-term-defensible components yields roughly $700 billion to $1.15 trillion. Morningstar's independent fair-value estimate of approximately $780 billion ($63 per share) sits squarely within this band and is the most rigorous published bear-to-base anchor. The implication is stark: roughly $700 billion to $1 trillion of the $1.77 trillion price, on the order of 40 to 55 percent, is option value on outcomes not yet demonstrated, namely Starship at target marginal cost, orbital AI data centers at relevant scale, and xAI competing with OpenAI, Anthropic, and Google at the frontier [12][18][11].

5.2 Independent analyst views versus the demonstrated record

The dispersion of independent (non-syndicate) views is exceptionally wide and itself a signal of uncertainty. Oppenheimer initiated at Buy with a $190 price target (bullish) [43]. NYU valuation specialist Aswath Damodaran told CNBC on June 7, 2026 that SPCX is "too richly priced," valuing the equity at $1.25 trillion to $1.35 trillion against the $1.77 trillion price; he wrote that the AI total addressable market "(26 trillion)... push into fantasy land" and added that Starlink "carried the company in 2025" [45]. The prospectus TAM decomposes into roughly $870 billion for Starlink broadband, $740 billion for Starlink mobile, $600 billion for X advertising, $2.4 trillion for AI infrastructure, and $22.7 trillion for enterprise applications [2][1]. The enterprise-applications figure in particular illustrates why TAM should be treated as a marketing frame, not a forecast.

5.3 Revenue and financial trajectory by segment, and the path to profitability

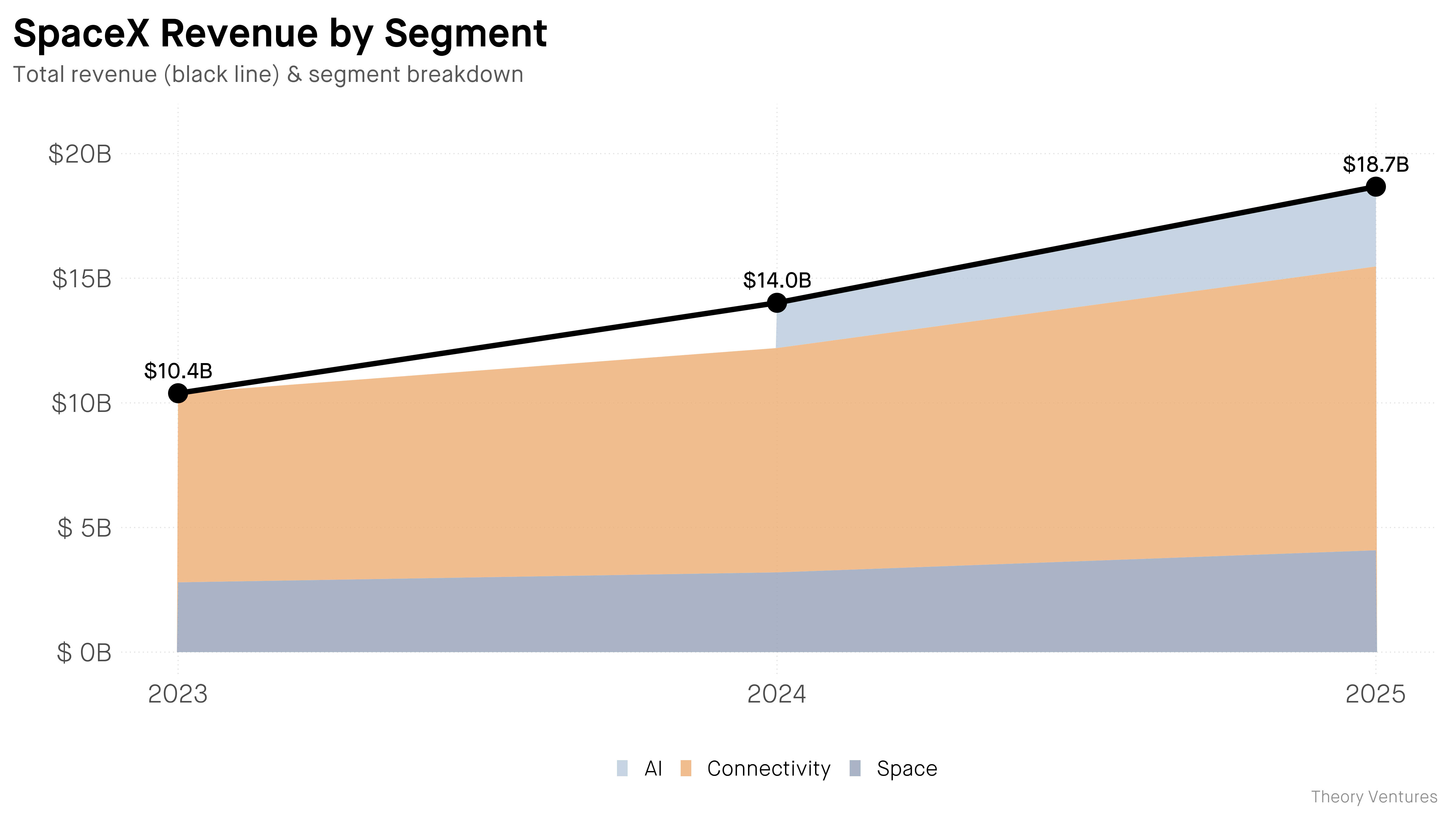

Consolidated 2025 results (prospectus disclosure): revenue of $18.7 billion, an operating loss of $2.6 billion, a net loss of $4.9 billion, and adjusted EBITDA of $6.5 billion [12][17]. Cumulative losses since inception reached approximately $41.3 billion [12]. First-quarter 2026: revenue of $4.7 billion, an operating loss of $1.9 billion, a net loss of roughly $4.3 billion, and adjusted EBITDA of roughly $1.1 billion [17][6]. The balance sheet carried roughly $12.1 billion of deferred revenue, of which about a third is recognized within twelve months [19].

A note on the growth rate: Morningstar reports recast revenue growth of 33 percent from 2024 to 2025, reflecting the consolidation of xAI and X; some independent estimates (for example Sacra) cite roughly 43 percent on a different basis [18][15]. The 33 percent figure is consistent with the prospectus recast and is used here, with the discrepancy noted.

The segment decomposition is the key to the profitability path. Connectivity is the growth engine and cash generator (61 percent of revenue, roughly 63 percent EBITDA margin) [12][14]. Launch is the strategic foundation but a modest, lower-margin contributor (22 percent of revenue, slight operating loss after Starship R&D) [14][15]. The AI segment is where capital intensity and losses concentrate: 17 percent of revenue but a roughly $6.4 billion operating loss in 2025 and the majority of group capital expenditure, and the loss is accelerating (per Data Center Dynamics, xAI "lost $2.4 billion in the three months to March 2026, up from $936 million a year ago") [16][17][2]. The credible path from a $4.9 billion net loss to the cash generation a $1.77 trillion valuation implies runs almost entirely through the AI segment: either xAI monetization scales rapidly to cover its capex, or capex moderates. Starlink and launch are already profitable; the consolidated loss is fundamentally an AI-investment loss [19][14]. GAAP profitability, required for eventual S&P 500 inclusion, is therefore gated on AI economics, not on the space business [41][43].

5.4 Addressable markets and scenario analysis (labeled as scenario reasoning, not forecast)

The following are explicitly scenarios, each with stated assumptions, not predictions.

Bull scenario. Assumptions: Starlink scales to 30 to 50 million subscribers with margins holding near current levels; an analyst illustration suggests roughly $18 billion of segment EBITDA at 30 million subscribers and $50 ARPU, and north of $25 billion at 50 million subscribers and $40 ARPU [19]. Starship reaches reliable reusability at low marginal cost within two to three years, unlocking orbital data centers and a vastly larger launch market. xAI competes at the frontier and monetizes Grok and X. Under these conditions the demonstrated-value base re-rates higher and the optionality begins to convert to cash, supporting valuations well above the IPO price over a decade; this is the territory of the Baron thesis, which remains assumption-dependent and unproven [44][19].

Base scenario. Assumptions: Starlink continues to compound but with ARPU pressure and rising competition; Starship matures over several years with intermittent setbacks (consistent with the Flight 12 booster loss); AI losses persist as capex stays elevated [21][14]. The stock is supported by index-inclusion flows and Starlink cash generation but is exposed to multiple compression from the roughly 95-times-sales starting point. Independent first-90-day scenario work (TradingKey) framed a week-one range of roughly $140 to $175, a month-one range of $130 to $165, and a three-month range of $120 to $200, contingent on Q2 Starlink subscriber data and xAI capex trends [12].

Bear scenario. Assumptions: Starship schedule slips materially; AI capex continues without commensurate revenue; ARPU erosion and competition compress Starlink margins; sentiment toward the founder deteriorates. Morningstar's $600 billion to $800 billion bear-case band implies downside on the order of 55 to 65 percent from the IPO valuation [18][12]. Historical precedent is cautionary: Facebook's 2012 IPO used a staggered lockup and shares fell more than 40 percent from the offer price before the lockup concluded [42].

5.5 Post-IPO public-market dynamics

Four mechanics will dominate near-term price action. First, lockup-expiry overhang: the staggered schedule begins releasing insider supply as early as the late-July Q2 earnings window, far sooner than a conventional 180-day cliff, and a 5 percent friends-and-family tranche can sell from day one [40][42]. Second, quiet-period and initiation effects: syndicate analysts cannot publish until the quiet period lapses, after which a wave of coverage (already foreshadowed by Oppenheimer's Buy and Morningstar's bearish read) will shape sentiment [43][18]. Third, float and index flows: the roughly 4 percent float plus forced passive buying from MSCI (June 13), Russell (about five days post-IPO), and Nasdaq-100 (about July 7) inclusion create a structural demand tailwind against thin supply, amplifying volatility in both directions [12][41]. Fourth, first-day and early behavior: pre-open indications of $169 to $175 and the "on course to blow past $2 trillion" framing suggest a meaningful first-day premium, but the realized close and any LULD halts must be taken from post-close data of record (Section 2.5) [4][3][2].

6. Regulatory Landscape

6.1 Launch licensing and environmental review

SpaceX operates under FAA Office of Commercial Space Transportation vehicle operator licenses, with launch cadence and trajectory changes subject to National Environmental Policy Act review [46]. For Starship at Boca Chica (Starbase), the FAA issued a Final Tiered Environmental Assessment and a Finding of No Significant Impact in February 2026 authorizing up to 25 Starship/Super Heavy launches and landings per year, while emphasizing that environmental review is only one part of licensing and that safety, risk, payload, and financial-responsibility reviews remain [48][46]. A separate Environmental Impact Statement for Starship operations at Kennedy Space Center Launch Complex 39A contemplates up to 44 launches and 44 landings per year [47]. Environmental litigation risk persists: local environmental-justice groups have challenged the "no significant impact" findings [48]. Each post-mishap investigation (such as the Flight 12 booster loss) is an FAA-overseen process that can gate return-to-flight [21][22].

6.2 Spectrum and market access

Starlink depends on FCC spectrum authorizations and international coordination through the ITU. The company began 2026 with roughly 9,500 satellites and FCC approval for an additional 7,500, and has sought authority for far larger constellations (up to 42,000 satellites have been discussed) [29][32]. The EchoStar AWS-4, H-block, and AWS-3 acquisitions required FCC approval; the FCC cleared the major transfer with conditions, and an escrow dispute remains a live item [35]. Market access abroad is a recurring friction point, with several governments seeking sovereign alternatives to a U.S. provider (Section 7) [29].

6.3 Export control, orbital debris, and space traffic

Launch vehicles and many satellite technologies fall under ITAR and related export-control regimes, constraining technology transfer and foreign sales. On orbital debris and space-traffic management, SpaceX's dominance is itself a systemic factor: Starlink satellites performed 144,404 collision-avoidance maneuvers between December 2024 and May 2025 (regulatory-filing figure), and SpaceX operates roughly two-thirds to three-quarters of all active maneuverable satellites [31][14]. The proliferation of competing megaconstellations raises conjunction risk, and coordination with Chinese constellations is described by experts as the principal unresolved gap [31].

6.4 New public-company obligations

Listing imposes Securities Exchange Act reporting: quarterly (10-Q) and annual (10-K) filings, Sarbanes-Oxley internal-control attestation, Regulation FD disclosure discipline, and insider-trading and Section 16 reporting. The first public earnings report, expected in the second half of 2026, will be the first audited window into segment performance as a public company and a key valuation catalyst [12]. As a controlled company, SpaceX relies on Nasdaq governance exemptions, reducing the independent-board protections public shareholders would otherwise have [1].

7. Geopolitical and Strategic Dimensions

7.1 National security dependence on a single provider

The United States' national-security and civil-space architecture is heavily concentrated in SpaceX. One analysis estimated that roughly 60 percent of DoD satellites deployed between 2022 and the end of 2024 used SpaceX's satellite bus, and that SpaceX's share of global spacecraft deployment approached 71 percent over the same period [38]. SpaceX flew 11 of 12 NSSL missions in 2025 [19]. This concentration is a double-edged strategic fact: it delivers capability quickly and cheaply, but it creates a single point of dependence on one company controlled by one individual, a concern explicitly voiced within government (Northrop Grumman was brought in as a partner on NRO work partly because "it is in the government's interest to not be totally invested in one company run by one person") [37].

7.2 Starshield and Starlink as strategic assets

Starshield, the militarized variant of Starlink, supplies the NRO's proliferated reconnaissance constellation (a reported 116 to 183-plus satellites), the Space Force's emerging MILNET data-transport layer, and Space Development Agency programs [36][37][39]. The Space Force's Proliferated LEO program carries a contract ceiling of $13 billion over ten years [39]. The exact wiring between the public Starshield offering and classified architectures is not fully public, a gap that will persist [36].

7.3 Competition from China and state-backed constellations

China is the most consequential competitive and geopolitical threat. State-backed megaconstellations include Guowang (13,000 satellites planned, roughly 80 launched), Qianfan/"Thousand Sails" (15,000 planned, roughly 90 launched), and Honghu-3, totaling a planned roughly 38,000 satellites [30][32]. China's launch cadence (over 90 orbital launches in 2025) and its progress toward reusable boosters bear watching, though both remain well behind SpaceX [28][30]. Commercially, Amazon's Leo (formerly Project Kuiper) is the most credible Western challenger, with roughly 3,236 satellites planned, a July 2026 FCC deadline to deploy 1,613, and a multi-vehicle launch procurement exceeding $10 billion; it had launched roughly 212 satellites by February 2026 [29]. Eutelsat OneWeb, Telesat Lightspeed, and the EU's IRIS² compete primarily on sovereign demand, where, as one industry executive put it, "there are lots of customers on the government side that do not necessarily want to use a U.S. supplier" [29]. The competitive picture in LEO broadband is shifting from a Starlink monopoly toward a genuine race, though SpaceX retains a commanding lead in scale, cost, and cadence [29][32].

7.4 Spectrum and orbital-slot geopolitics

Spectrum and orbital slots are finite and contested. SpaceX's aggressive spectrum acquisition (EchoStar) and large filings strengthen its position but intensify international coordination disputes, particularly with state-backed Chinese operators that view their constellations as strategic national assets [32][29]. This sub-dimension is real but is substantially subsumed by the spectrum (Section 6.2) and competition (Section 7.3) discussions and is not padded further here.

8. Risk Matrix

| Risk | Likelihood | Impact | Mitigation |

|---|---|---|---|

| Valuation / multiple compression (roughly 95× trailing sales) | High | Severe share-price downside if growth expectations are not met; independent valuation work implying substantial downside versus IPO valuation. | Few structural mitigations; continued execution on Starlink growth, Starship operations, and AI monetization would be the primary offsets. |

| Lockup-expiry / float overhang | High (6–12 months) | Moderate-to-severe near-term price pressure as additional shares enter the market. | Staggered release structure and potential index-inclusion demand may partially offset selling pressure; founder lockups may signal alignment. |

| First-day / near-term volatility | High | Moderate impact; limited public float can amplify swings, volatility interruptions, and price discovery challenges. | Index-related demand may provide partial support; investors typically manage through position sizing and time horizon discipline. |

| Dual-class governance / founder concentration | Certain (structural) | Moderate-to-severe; public shareholders have limited influence over governance, capital allocation, and board decisions. | No direct mitigation for shareholders; reliance on founder restraint, board governance practices, and internal controls. |

| Key-person risk (founder) | Moderate | Severe reputational, political, operational, or legal exposure tied to leadership concentration. | Experienced executive bench, diversified business units, and succession planning help reduce but do not eliminate risk. |

| Starship technical / schedule risk | Moderate to High | Severe impact on long-term growth thesis if development timelines slip or technical setbacks persist. | Iterative testing programs, regulatory approvals, large engineering teams, and extensive flight-test campaigns. |

| Customer / revenue concentration (U.S. government) | Moderate | Moderate-to-severe exposure to changes in NASA, DoD, or intelligence-community procurement priorities. | Diversification into commercial, enterprise, consumer, and international revenue streams; backlog growth. |

| xAI integration / disclosure risk | Moderate | Severe earnings pressure if AI-related operating losses continue to expand faster than revenue growth. | Cash-flow generation from mature businesses; external AI contracts; eventual monetization of AI infrastructure. |

| Regulatory / environmental delay | Moderate | Moderate impact; environmental reviews, litigation, or investigations may constrain operational cadence. | Multi-site development strategy, regulatory engagement, and permitting diversification. |

| Competitive erosion of Starlink | Moderate, rising | Moderate long-term pressure from competing satellite constellations and declining average revenue per user. | Vertical integration, spectrum assets, launch-cost advantages, and expansion into direct-to-device services. |

| Capital intensity / path out of losses | High (near term) | Moderate-to-severe; large ongoing capital expenditures and cumulative losses require continued funding. | Growth in launch and satellite-service profitability; moderation of AI capital spending; access to IPO proceeds and capital markets. |

| Political / reputational exposure affecting contracts | Moderate | Moderate-to-severe; public controversies or political developments could influence customer and government relationships. | Mission-critical role within national space infrastructure may reduce the likelihood of abrupt contract termination. |

9. Strategic Recommendations

9.1 For retail investors and prospective or new shareholders (this is not investment advice)

The following is analysis to inform your own judgment and is explicitly not personalized investment advice.

Treat SPCX as a richly valued, newly public stock whose first six months will be dominated by mechanics, not fundamentals: a roughly 4 percent float, forced index-inclusion buying, a staggered lockup that begins releasing supply as early as the late-July Q2 earnings window, and a syndicate quiet period that delays independent initiations [40][41][43]. Recognize the dual-class structure: owning Class A confers economic exposure but essentially no control [1].

Stage your thinking around leading indicators that would confirm or undermine the thesis: (1) Starlink subscriber additions and ARPU at the first public earnings report (above roughly 11 million subscribers by Q2 would support the bull path; continued ARPU erosion without margin offset would not) [12][19]; (2) Starship progress toward repeatable booster recovery and first operational Starlink payloads in the second half of 2026 [22]; (3) the trajectory of AI-segment losses and capex, the single largest swing factor in the path to GAAP profitability [17][14]. Let the bull, base, and bear scenarios (Section 5.4) calibrate expectations: the base and bear cases both imply meaningful downside risk from the IPO valuation, so general prudence favors modest position sizing, awareness that lockup tranches can pressure the stock, and patience for post-lockup, post-initiation entry points rather than chasing a thin-float first-day premium [42][18]. None of this is a recommendation to buy or sell; it is a framework for your own analysis.

9.2 For aerospace and space-sector professionals and strategists

A publicly traded SpaceX with a roughly $1.77 trillion equity currency and a public cost of capital changes the competitive landscape materially. Expect SpaceX to use stock as acquisition currency (the EchoStar spectrum deals, partly stock-funded, are a template) and to press its cost advantage harder [35][33]. The demonstrated capability gap in launch is widening, not narrowing: 165 Falcon launches in 2025, a 99.6% Falcon family success rate, and booster reuse past 35 flights set a cadence and reliability bar competitors cannot currently approach [27][26]. The gap in LEO broadband is beginning to narrow at the margins as Amazon Leo and Chinese constellations scale, but SpaceX's vertical integration, in-house silicon, and spectrum moat preserve a multi-year lead [29][33].

Strategic implications: (1) launch customers and satellite operators should plan for a world in which Starship, if it reaches target economics, compresses cost-per-kilogram by another order of magnitude, which would reset the business case for large constellations, in-space manufacturing, and orbital compute [25][24]; (2) suppliers and competitors dependent on government demand should note the concentration risk the government itself is flagging, which may create deliberate second-source opportunities (the Northrop Grumman NRO partnership is the model) [37][38]; (3) adjacent businesses (ground systems, D2C handset ecosystems, space-traffic management, defense data transport via MILNET) will be shaped by SpaceX's roadmap and should position accordingly [39][31].

9.3 Note for space-exploration enthusiasts

The listing does not change the long-duration exploration agenda, and that is the analytically important point. Founder supermajority control, reinforced by a compensation plan that ties 200 million super-voting shares to a $7.5 trillion valuation and a one-million-person Mars colony, and 60.4 million additional shares to operating 100-terawatt space-based data centers, insulates Mars and deep-space programs from public-market pressure for near-term returns [49][50]. Public capital is explicitly intended to fund the Starship scale-up and orbital-compute layer that a Mars supply chain would require [50]. Enthusiasts should read crewed-Mars dates as founder aspiration, not schedule, and watch the demonstrated gates instead: repeatable Starship reuse, orbital propellant transfer, and the uncrewed HLS lunar demonstration [21][22].

10. Caveats

This analysis treats the IPO as a completed fact and anchors confirmed terms on the SEC Form S-1 and primary reporting of record [1][2][5]. Several figures carry lower confidence and are flagged in text: Falcon 9 marginal cost and refurbishment figures are founder-asserted or analyst-modeled, not audited prospectus disclosures [25][24]; the realized first-day opening, intraday range, and closing price were not yet published at the time of writing and must be taken from post-close data of record [2][3]; reported revenue-growth rates differ between the prospectus recast (33 percent) and some independent estimates (about 43 percent) because of xAI/X consolidation [18][15]; and the $250 billion implied xAI value derives from merger-transaction reporting rather than a standalone audited valuation [9][10]. Total-addressable-market figures are prospectus marketing frames, not forecasts, and should be discounted heavily [45][1]. Scenario analysis in Section 5.4 is explicitly assumption-driven reasoning, not prediction. Forward-looking management goals (Starship cadence, orbital data centers, crewed Mars) are labeled as stated goals throughout and assessed against the demonstrated record. Where independent and company figures conflict, the conflict is noted rather than silently resolved.

References

[1] Space Exploration Technologies Corp. 2026. "Form S-1 Registration Statement." U.S. Securities and Exchange Commission, May 20.

[2] CNBC. 2026. "SpaceX (SPCX) IPO: Live Updates." June 12.

[3] Reuters (Saini, Manya, Echo Wang, and Niket Nishant). 2026. Coverage of SpaceX market debut, via Investing.com. June 12.

[4] NBC News. 2026. "SpaceX Shares Set to Surge 30% in Largest IPO Ever." June 12.

[5] Nasdaq. 2026. "SpaceX (SPCX): Rocket Company Launches Historic IPO." June 12.

[6] CNN Business. 2026. "Live Updates: Investors Await First Trade in SpaceX Market Debut." June 12.

[7] NPR. 2026. "SpaceX Blasts Off with a Record-Breaking $75 Billion IPO." June 11.

[8] Fortune. 2026. "SpaceX's IPO Could Be Largest in History. Here's How It Compares." June 12.

[9] CNBC. 2026. "Musk's xAI, SpaceX Combo Is the Biggest Merger of All Time, Valued at $1.25 Trillion." February 3.

[10] Bloomberg. 2026. "Musk's SpaceX Combines with xAI at $1.25 Trillion Valuation." February 2.

[11] NBC News. 2026. "Markets Will Soon Test a Musk Merger That Promises 'Space-Based Internet'." February. (Del Deo capex estimates via Light Reading, 2026.)

[12] TradingKey. 2026. "SpaceX IPO Debuts at $135 at a $1.75 Trillion Valuation on June 12." June 12.

[13] KraneShares. 2026. "SpaceX IPO: 5 Key Takeaways from the S-1 Filing." May.

[14] Tunguz, Tomasz. 2026. "SpaceX's Limitless Ambition: An AI Conglomerate." May.

[15] Sacra. 2026. "SpaceX Revenue, Valuation & Funding."

[16] Via Satellite. 2026. "SpaceX's IPO Filing Gives First Look into Company's Financials." May 20.

[17] Trending Topics. 2026. "The SpaceX IPO Prospectus: 15 Key Insights from the S-1 Filing." May.

[18] Morningstar. 2026. "6 Charts on SpaceX's Pre-IPO Financials."

[19] Mostly Metrics. 2026. "SpaceX S-1: Starlink Revenue, Launch Margins, Musk's Mars Pay."

[20] Wikipedia. 2026. "List of Starship Launches." Accessed June.

[21] CNN. 2026. "SpaceX Scrubs Attempt to Launch Amped-Up Starship V3 on Inaugural Test Flight." May 21.

[22] NPR. 2026. "SpaceX Launches Its Biggest, Most Beefed-Up Starship Yet on a Test Flight." May 23.

[23] SpaceNews. "SpaceX's Reusable Falcon 9: What Are the Real Cost Savings for Customers?"

[24] ARK Invest. "The Turnaround Time in Rocket Reuse Suggests the Cost of Refurbishing the First Stage of the Falcon 9 Has Dropped from Roughly $13 Million to $1 Million." Newsletter Issue 335.

[25] Inverse. "SpaceX: Elon Musk Breaks Down the Cost of Reusable Rockets."

[26] Wikipedia. 2026. "Falcon 9" and "List of Falcon 9 and Falcon Heavy Launches." Accessed June.

[27] Space.com. 2026. "SpaceX Shatters Its Rocket Launch Record Yet Again: 165 Orbital Flights in 2025."

[28] SpaceNews / Space Economy Institute. 2026. "Record Launches in 2025, as SpaceX Prepares a 'Heavy' Turning Point." January.

[29] Via Satellite. 2026. "The Coming Wave of Competition in LEO Constellations." March.

[30] Space.com. "China Launches 8th Batch of Satellites for 13,000-Strong Internet Megaconstellation."

[31] Aerospace America (AIAA). "Heavy Traffic Ahead."

[32] Technology Magazine. "Starlink Faces New Rivals in Satellite Internet Market."

[33] CNBC / Data Center Dynamics. 2025. "SpaceX Buys Wireless Spectrum from EchoStar in $17 Billion Deal." September 8.

[34] EchoStar Corporation. 2025. "EchoStar Announces Spectrum Sale and Commercial Agreement with SpaceX," Form 8-K Exhibit 99.1. SEC, September 8.

[35] SpaceNews. 2025. "EchoStar Sells More Direct-to-Device Spectrum for Bigger SpaceX Stake." November 6.

[36] New Space Economy. 2026. "What Is SpaceX Starshield, and Why Is It Important?" March 27.

[37] Wikipedia. "SpaceX Starshield." Accessed June 2026.

[38] Ill-Defined Space. "Picking a Proven Winner: NRO and Starshield."

[39] Breaking Defense. 2025. "Space Force Is Contracting with SpaceX for New, Secretive MILNET SATCOM Network." June.

[40] CNBC. 2026. "SpaceX Insiders Will Get to Sell Shares Earlier Than Usual After the IPO." May 21.

[41] InvestmentNews / Friedman, Jacob. 2026. "SpaceX's Index Fund Debut Will Look Nothing Like What Most Investors Expect."

[42] Investing.com. 2026. "SpaceX Guide: Everything You Need to Know About the Biggest IPO in History."

[43] Kiplinger. 2026. "SpaceX IPO: Live Updates and Commentary." June 12.

[44] The Motley Fool. 2026. "Billionaire Ron Baron Believes SpaceX Will Be Worth $30 Trillion by 2040." June 11.

[45] Benzinga / CNBC. 2026. "Elon Musk Reacts to $30 Trillion SpaceX Valuation Call: 'Ron Is Smart'"; and Aswath Damodaran CNBC commentary, June 7.

[46] Federal Aviation Administration. 2026. "Final Tiered Environmental Assessment and FONSI/ROD, SpaceX Starship-Super Heavy, Boca Chica Launch Site."

[47] Federal Aviation Administration. 2025. "Final Environmental Impact Statement and Record of Decision, SpaceX Starship-Super Heavy at Kennedy Space Center Launch Complex 39A."

[48] Teslarati / MyRGV. 2026. "SpaceX Secures FAA Approval for 25 Annual Starship Launches." February.

[49] Startup Researcher / Reuters. 2026. "SpaceX Ties Musk's Pay to Mars Colony and $7.5T Value."

[50] Fortune. 2026. "Elon Musk's Pay Package Reveals What SpaceX Actually Is: A $1 Trillion Monster Built to Colonize Mars." May 20.

[51] Fast Company. 2026. "SpaceX IPO Update: Latest SPCX Stock Price, Trading Start Time for Closely Watched Nasdaq Debut." June.

[52] The Motley Fool. 2026. "The SpaceX IPO Has an Unusual Lockup Policy for Insiders." May 26.

[53] Gautam, Abhishek. 2026. "SPCX Opens June 12: The Number Every AI Investor Is Watching."